#107: Kaspi: the growth strategy of Kazakhstan's super app

W FINTECHS NEWSLETTER #107: 20/05-26/05

👀 Portuguese Version 👉 here

This edition is sponsored by

Iniciador enables Regulated Institutions and Fintechs in Open Finance, with a white-label SaaS technology platform that reduces their technological and regulatory burden:

Real-time Financial Data

Payment Initiation

Issuer Authorization Server (Compliance Phase 3)

We are a Top 5 Payment Initiator (ITP) in Brazil in terms of transaction volume.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

In 2021, I wrote about how the super app strategy can work in some markets and not in others. What we have observed around the world is that in emerging and developing markets, the adoption of super apps tends to be higher than in developed markets, such as the USA and the UK.

This is interesting because it demonstrates two things: (i) The first is related to the fact that the technological structure and consumer needs in emerging and developing markets are different. In these regions, integrating multiple services into a single app can be more convenient and attractive due to lower penetration of high-end devices and the pursuit of more accessible and comprehensive solutions. (ii) The second is linked to consumer behavior in developed markets, where there is greater service segmentation and a preference for specialized apps, each fulfilling specific functions more efficiently.

We have great examples from emerging markets, such as WeChat in China, Kakao in South Korea, Kaspi in Kazakhstan, among others. I've previously covered each of these apps here.

The story of Kakao is available in Portuguese 👉 here;

The story of WeChat is available in Portuguese 👉 here;

Although Asia is a reference in super apps, some players face challenges in adapting their business models to ensure sustainable growth in the future. Several prominent companies, such as Paytm in India, Ant Group in China, and Kakao in South Korea, are facing regulatory challenges due to violations and improper practices in the market, which directly affect their fintech operations.

Paytm, for example, faces the potential loss of its payment license, while Ant Group is dealing with increasing regulatory crackdown that has decreased its valuation and resulted in Jack Ma stepping down from controlling the company. Kakao has also faced allegations of stock manipulation.

Kaspi.kz is a good example of a super app that has also been scaling, although it has had its dark moments throughout its history. Recently, it became the first company based in Kazakhstan to be listed in the USA. Its Nasdaq debut was quiet, with shares closing just 0.5% above the offering price of $92. Now with broader fundraising, Kaspi.kz aims to expand to 100 million users; it currently has 13.5 million customers. Nearly 70% of Kazakhstan's population of 20 million people use the company's super app in some form.

With the user perspective market saturated, Kaspi.kz aims to be central in how people buy and pay for goods, as well as manage their personal finances. Out of 2 million small and medium-sized merchants, 580,000 of them accept payments from Kaspi.kz. The company has benefited from several favorable winds in recent decades.

In 2021, I wrote about the country and how the company was revolutionizing the market in Kazakhstan. At the time, I had mapped out 20 Super App players and how they were gaining traction. It's interesting to revisit where these players were from: China, India, Brazil, Russia, and South Korea, even though it's not a developing country anymore, it has a remarkable history with the financial system (I wrote about it in this edition, in Portuguese 👉 here).

Below is the complete 2021 edition #16 about Kaspi and Kazakhstan 👇👇

In the last edition, we discussed how super apps are related to the level of economic development of the countries where they exist [available here]. China and India are among the biggest success stories in this category. However, there are other examples that were not explored in that article, with Kazakhstan being one of them, with Kaspi.

Kazakhstan has an intriguing history. Situated in Central Asia and a member of the former Soviet republic, the country shares borders with China and Russia. Since its independence in 1991, Kazakhstan has shown significant economic growth primarily due to its oil trade.

When the USSR (Union of Soviet Socialist Republics) dissolved, Central Asia was reformed with the emergence of countries like Kazakhstan, Uzbekistan, Turkmenistan, and Tajikistan, transforming Central Asia into a new and independent region. After nearly a century under communist precepts, the newly formed states needed to deal with a new level of capitalism and market economy. Unprepared, they were destined to economically depend on the powers of the region — especially Russia — until they could diversify their productions and compete in this new reality.

However, the abundant existence of oil was enough to change this forecast.

Oil and natural gas play a crucial role in Kazakhstan's economy, accounting for over 17% of GDP in 2013. Among the former Soviet republics, it is the second-largest oil producer. Although Kazakhstan has been producing oil since 1911, it wasn't until the mid-1990s, with the entry of major international oil companies, that a true development in oil extraction and production volume was witnessed.

The presence of oil made the country stand out in international trade and attracted the attention of international investors. The reasons why emerging countries assumed a new position on the international stage, to the point of being able to threaten the status of the world's major powers, are rooted in economic globalization and the importance their economies began to exert in this process — primarily in oil exports.

However, since the 2008 crisis, which highlighted Kazakhstan's economic dependence on its oil exports, resulting in a dramatic reduction in its GDP growth rate, economic diversification has proven necessary for the country to become less sensitive to shocks in its trade balance and, mainly, to the effects generated by a possible crisis in the main countries that import its oil. Thus, in 2010, the local government launched the 2020 Development Plan, whose objectives were primarily to reduce dependence on the extraction and export of raw materials and ensure increases in productivity.

Digital Transformation

Since then, the country has experienced significant increases in investment in industry and technology. Digital transformation is another movement that is present in the country.

With a percentage of internet users exceeding 81% of the population, the Kazakhstan Digital Program tends to further accelerate inclusion and digital transformation in the country. The Program has five main objectives:

Digitization of economic sectors - reorganizing traditional economic sectors using technologies and new possibilities that increase labor productivity and lead to capitalization growth;

Transition to the digital state - transforming the state infrastructure to provide businesses and services to the population, anticipating their demands;

Implementation of Silk Way Digital - development of high-speed and secure infrastructure for data transfer, storage, and processing;

Evolution of human capital assets - transformational changes, including the formation of a creative society and the transition to new realities - a knowledge-based economy;

Formation of ecosystems - developing technological entrepreneurship, with stable relationships between companies, academia, and the state, as well as introducing innovations in the industry.

Kazakhstan has also initiated a project to ensure access to fiber optic broadband in rural settlements in the country. Another project is the construction of 3G/4G mobile networks in rural settlements, aimed at increasing connectivity through collaboration between the Government and private providers.

This digital transformation has helped pave the way for the emergence of super apps.

The Kaspi Super App

The story begins in 1993 with a young man, Vyacheslav Kim, living in the capital of Kazakhstan. Instead of entering the corporate world dominated by the oil industry, the graduate of Almaty State University started a business at the age of 23. Planet Eletroniki was an electronics supplier, a kind of Casas Bahia of Kazakhstan.

In no time, the store turned into one of the largest retailers in Kazakhstan. Throughout his entrepreneurial journey, Kim realized that one of the factors limiting the sale of his products was financing options. At that time, after the dissolution of the USSR, the country saw its per capita GDP shrink slightly; the population gradually lost its purchasing power while adapting to the new economic model.

To overcome this barrier, retailers turned to M&As and began acquiring banks with the main goal of providing loans to buyers. Kim was one of them. In 2002, the entrepreneur acquired Kaspiskiy, which had recently been privatized. In a company statement in July 2019, Kim said:

"It may have been a bit naive, but buying a bank was a big trend. Every successful entrepreneur was buying a bank, so we did too."

However, Kim had difficulties leveraging his new business. The lack of synergy with Planet and the employees present in the bank — with a culture not compatible with the one desired by the entrepreneur — were some of the factors limiting the success of his new asset. Kim then sought partners with experience to bring to his new business.

New partners

After Kim's departure from Planet in 2000, the entrepreneur was focused on his new venture. But it was in 2006 that things began to change. When an investor, Michael Calvey, an American founder of Baring Vostok, a Russian investment company, decided to invest in Kim's new business, he brought not only money (which has not been disclosed to this day), but also brought a young man from Georgia, a dreamer who had a clear purpose of positively impacting people's lives. That young man was Mikhail Lomtadze, the current CEO of the company.

Lomtadze had such grand plans for his career that he was willing to make some sacrifices. After graduating from Harvard Business School in 2002, Lomtadze met the founder of Baring Vostok in New York. In his first conversation with Calvey, he said, "I don't need a salary." When Calvey decided to invest in Kim's bank, Kaspisky, Lomtadze was already a project investment manager at Calvey's company, and when he was introduced to Vyacheslav Kim, it was "love at first sight."

In an interview with PWC, when asked what had led him to success, Lomtadze said:

"If it weren't for Vyacheslav, his faith, friendship, support, and teamwork, none of this would have been possible. From the beginning, 14 years ago, we believed in each other, decided to become partners, and establish a cool company that we could be proud of. We didn't even formalize the partnership between us on paper until the last moment. This is only possible when there is complete trust and chemistry. […] As you noticed, I've been in Kazakhstan for 14 years, and this period is almost my entire professional life. All this time, Vyacheslav Kim has always supported me.", available here

After Lomtadze's arrival, the bank underwent a rebranding, changing from Kaspisky to Kaspi. Today, Kaspi's banking and mobile payment app is used by about half of Kazakhstan's 18 million inhabitants, and in less than a decade, the company has helped reduce the use of cash in the country. Kaspi claims to now be responsible for 68% of all electronic transactions in Kazakhstan, nearly double the size of all its competitors combined, including Visa and Mastercard. During the COVID-19 quarantine, the company was responsible for providing social assistance to more than 4.5 million people. Every 2 out of 3 money transfers occurred with the help of Kaspi's Super App.

Business Model

When the company went public on the London Stock Exchange, it was considered the largest IPO outside Kazakhstan. But how does its super app work?

Kaspi's Super App platform has three main segments: payments, marketplace, and loans (which they call fintech).

Currently, Kaspi has half of its business dominated by the lending segment. Compared to 2020, there has been growth in its payment platform and marketplace — largely driven by pandemic consumption.

38% of its consumer base uses all three products of the platform; 40% of merchants use its payment and marketplace products [full presentation here].

With the growth in the number of users during the year 2020, the super app began offering other services in December 2020, such as travel services. Today, this new service already has a 26% market share in airline ticket sales.

Additionally, the company also committed to helping the government control COVID-19 cases (the GovTech part of the app). Being the largest Super App in the country and on the smartphones of millions of people, Kaspi launched a functionality during the pandemic that allows for monitoring coronavirus cases. This feature has 3.4 million Monthly Active Users (MAU).

Kazakhstan: Fertile Ground for Super Apps

The Kazakhstan market has proven to be fertile ground for a Super App for several reasons:

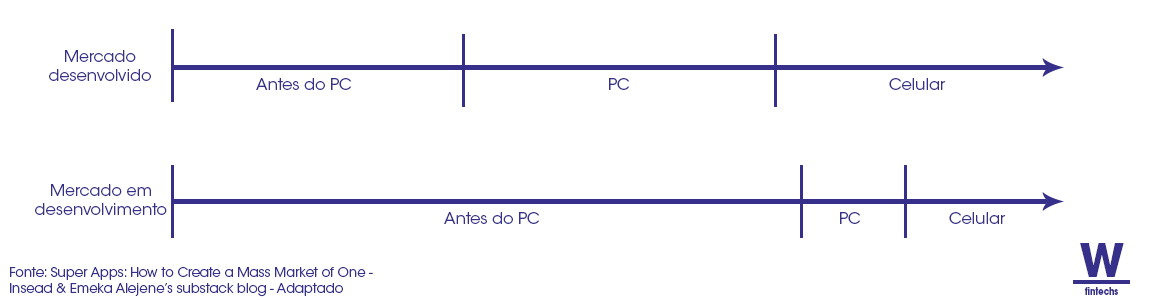

Firstly, due to the sudden inclusion of the population on the internet. Kazakhstan's history meant that the arrival of the computer industry took a little longer to establish itself in the country, resulting in brief contact with PCs;

The network effects generated by the payment functionality led to money transactions being replaced in the country. Today, almost any type of cash transaction between individuals can be facilitated by the Kaspi app (paying for a taxi ride, paying for a restaurant);

Kazakhstan's nascent banking structure and low levels of trust due to the number of bankruptcies of local banks, fraud, etc., made Kaspi's app a success — and its main vertical was lending (fintech).

Final thoughts

Kaspi's story is similar to that of Casas Bahia in one sense: its lending side. Kim, despite leaving Planet Eletroniki, was visionary in seeing the size of the lending market at that moment when Kazakhstan entered the market economy. During the 1950s, when Casas Bahia began offering credit to its consumers, we also had a nascent Financial System. The institutional reforms of the PAEG (Government Economic Action Program), during the first military government, were the beginning of part of the SFN we have today — I'll leave that story for another day. When the Central Bank didn't even exist in Brazil, a retailer became one of the largest financiers in the country [I talked about the history of Casas Bahia, as well as BNPL, here].

Entrepreneurs in Kazakhstan saw the same opportunity. With an extremely new Financial System and not yet accustomed to the new variables of the capitalist economy, retailers began to look favorably upon providing loans for their consumers' purchases. Kaspi is the result of all this. It represents a moment of transition in production; it represents a moment of modernization of its banking system, but, mainly, it represents a moment where previously irrelevant countries became relevant because of their innovation. As I said in the last edition, the Super App is a new opportunity for developing countries to overcome their challenges. Let us, Brazilians, overcome ours.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.