#110: The landscape of digital wallets in Latin America

W FINTECHS NEWSLETTER #10: 08/07-14/07

👀 Portuguese Version 👉 here

This edition is sponsored by

Iniciador enables Regulated Institutions and Fintechs in Open Finance, with a white-label SaaS technology platform that reduces their technological and regulatory burden:

Real-time Financial Data

Payment Initiation

Issuer Authorization Server (Compliance Phase 3)

We are a Top 5 Payment Initiator (ITP) in Brazil in terms of transaction volume.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

A few months ago, I wrote here that Peru and other countries in the region were seeking greater interoperability between their digital wallets as a way to further boost the adoption of digital payments in their payment infrastructures. Payments often serve as the gateway to financial inclusion and citizenship.

India has been transformed by UPI, Thailand by PromptPay, Brazil by Pix—used by 80% of Brazilians, 13 million businesses, and 800 participating institutions — but in other Latin American countries, there are still adoption challenges in their systems. In Mexico, the regulator has been trying to course-correct through overlay services. First, it was CoDi, now, it’s DiMo.

In Peru, many initiatives are progressing in favor of greater payment interoperability. In a study published by the Central Bank of Peru in June 2023, the search for more interoperability to improve the payment experience was highlighted. Currently, the payment landscape in the country is challenging. The main payment method in Peru is cash. According to data from the central bank of the country, until 2022 cash usage accounted for over 90% of payments for goods or services. However, despite this preference, the use of online or mobile banking services has been increasing. The study acknowledged that this improvement was due to access to fiber optics, which has doubled in the last 5 years. Digital wallets have also gained relevance in Peru since the pandemic, with the number of operations conducted through digital wallets from September 2022 being almost triple those conducted in the same month of 2021. The Central Bank expects the implementation of interoperability to significantly increase these numbers.

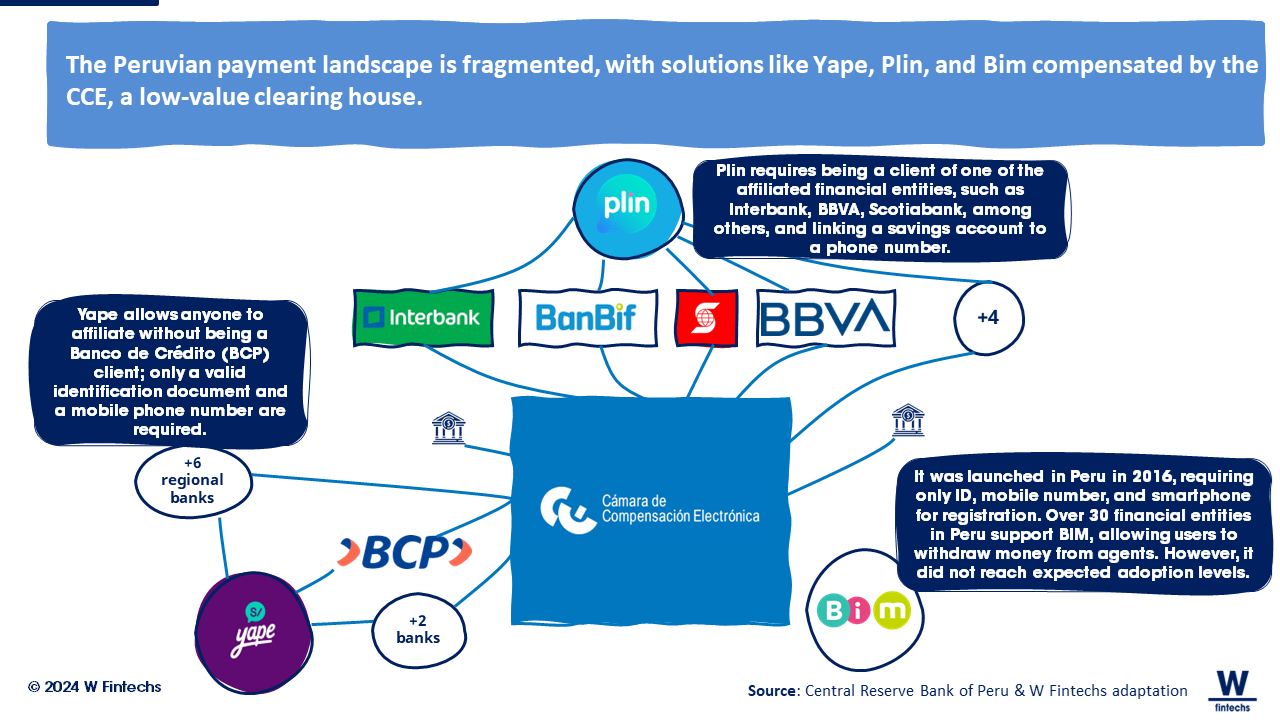

Despite this increase, Peruvians face a challenging user experience due to the proliferation of closed-loop solutions, such as Yape and Plin, operating in the card system, and BIM, an industry initiative that has not yet achieved the expected adoption. On the other hand, there is a regulated market compensation system for low-value transfers, represented by the Electronic Clearing House (CCE).

In Argentina, the central bank announced that any digital wallet can now make credit card payments using any QR code, with the application initiating the payment charging a 0.07% commission per transaction. The idea is to reduce the concentration that Mercado Pago has acquired in recent years — today, Mercado Pago has the highest fees for merchants.

The main difference between Mercado Pago and other players in Argentina is that Mercado Pago connects directly to the Visa and Mastercard networks, while other wallets need to pay for the link to acquirers. This has given it a significant competitive advantage.

Although more countries want to adopt systems similar to Pix, it is likely that more countries in the region will adopt these interoperability practices, as the digital wallet market has already proven to be an effective way for adoption by the population.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.