👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

This edition is sponsored by

Iniciador is the complete infrastructure platform specialized in Regulated Open Finance, enabling Payment Initiation and Data Access.

The solution removes technology and compliance concerns, allowing clients — with their own regulatory license or using Iniciador’s — to focus on new products and business growth.

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉 here

This is a Short Takes edition, and as the name suggests, it’s different from deep dives. In editions like this, I’ll explore various topics that could later develop into a full deep dive.

Typically, I’ll cover three key areas:

A reflection on the financial innovation market;

Something that caught my attention, whether a podcast, a launch, or a report;

News that stood out to me.

The idea is to publish editions like this at least once or twice a month.

In recent months, I’ve been analyzing three markets that, over time, are likely to become increasingly integrated: Data Analytics, Payments, and Digital Consumer.

Looking at last year’s numbers for the performance of these segments, it’s clear that Data Analytics companies are leading with higher multiples.

A few editions ago, I shared that financial institutions are becoming data companies, and the multiples and revenue growth of Data Analytics firms likely reflect the growing importance of data in decision-making, as well as the impact of AI and Machine Learning in the financial sector.

With an EV/Revenue multiple of 9.3x, the strong investor appetite for solutions that address data complexity is evident. Median revenue growth is 7.7%, and EBITDA margins range from 38% to 50%. These companies stand out for their ability to generate revenue and profitability, driven by increasing demand for solutions that simplify data analysis and utilization — personalization will undoubtedly become increasingly relevant in the strategies of banks and fintechs.

Payments, on the other hand, remains the heart of fintech. While it doesn’t experience the same explosive growth, with revenues growing between 6.6% and 12.8%, this is largely because it’s a sector that’s already well-priced, offering more stability and consistent operating margins.

The EV/Revenue multiple of 1.6x reflects this maturity, showing that it’s a more conservative market where innovation needs to be swift to stand out. One strategy some players have adopted is revenue diversification through integrated financial management solutions and value-added services. Despite this, payment companies have shown solid fundamentals and steady revenue streams, making them more attractive in terms of lower volatility.

The Digital Consumer segment presents significant potential but also higher risks, primarily due to its heavy exposure to macroeconomic conditions, including inflation and interest rates. Revenue growth ranging from 12% to 36% is promising, but EBITDA margins between -14% and 32% indicate that some companies are still struggling to deliver the expected profitability. Despite this volatility, the EV/Revenue multiple of 8.9x suggests the market is betting on the sector’s digitalization. I believe that emerging markets, especially those not yet partially digitalized, hold immense potential for growth.

At the end of the day, I believe these three segments will converge as parts of a larger puzzle, where data will not only be the fuel but also the mechanism driving financial innovation.

The numbers are based on aggregated indices from D.A. Davidson’s latest report, available 👉 here.

If you enjoyed this edition, share it with a friend. This will help spread the message and allow me to keep offering quality content for free.

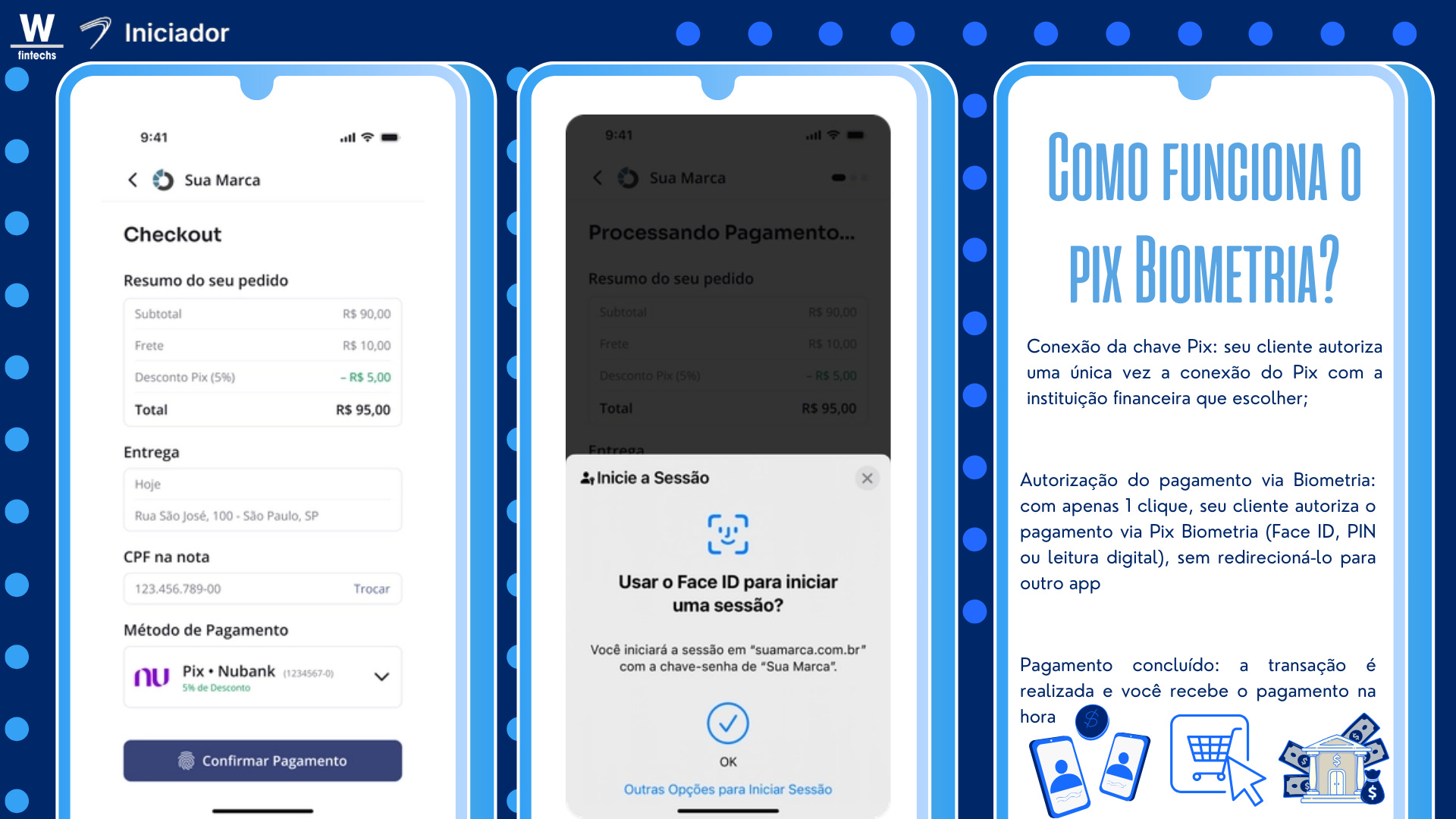

A few weeks ago, I shared a use case for Pix with Biometrics. From now on, digital payments will become even faster with the adoption of the FIDO (Fast Identity Online) protocol by the Central Bank. This means user authentication will happen directly on the device using biometrics — either fingerprint or facial recognition.

This evolution of Pix, built on the Open Finance infrastructure, is the perfect solution for payment service providers, digital wallets, marketplaces, platforms, and conversational payments.

For example, in e-commerce, customers can complete their purchases instantly and securely by using biometrics to validate the transaction, without any interruptions in the payment flow.

The Iniciador has already made this feature available for testing with the country’s largest banks: Itaú Unibanco, Nubank, C6 Bank, BTG Pactual, Mercado Pago, PagBank, Banco do Brasil, Sicredi, Digio, next, and Bradesco. You can test it too!

Simply fill out the form below with a few details to gain access to the No Redirection Journey 👉 here.

APIs are now available for integration in the SaaS model via White Label and SDK for browsers, as well as the Infra ITP product, available to authorized institutions. Just get in touch with the Iniciador team 👉 here.

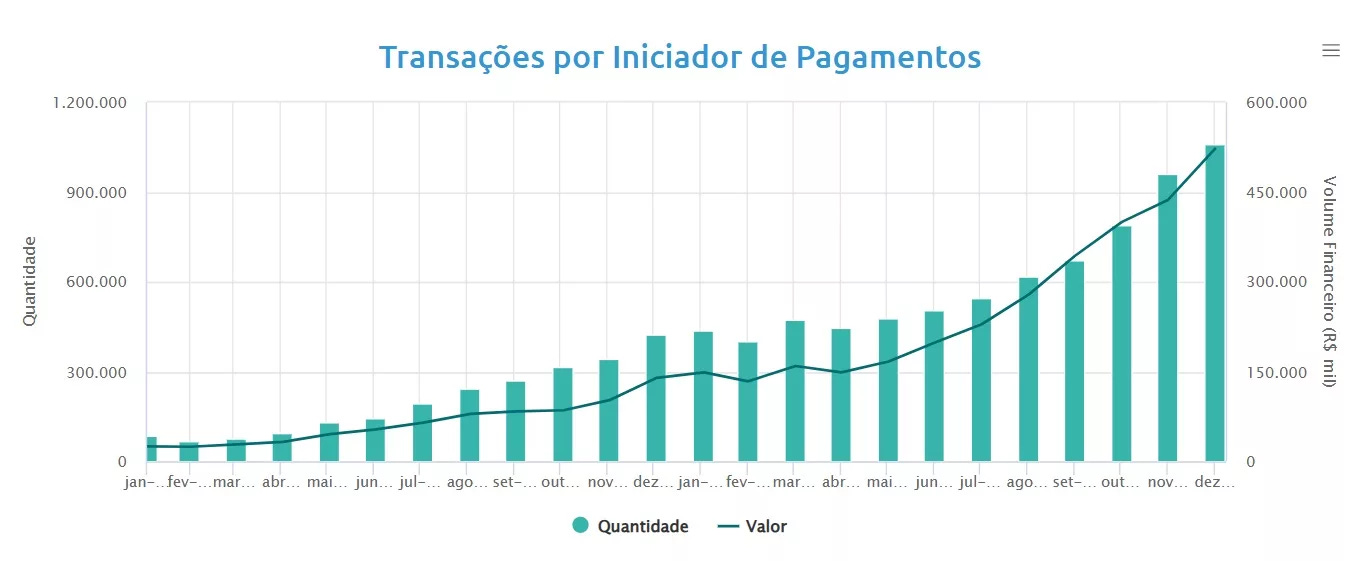

🇧🇷 Payment Initiation Hits Record R$3.2 Billion in 2024 - 👉Finsiders

“In 2024, payment initiation transactions via Pix totaled R$3.2 billion. This figure represents more than five times the R$624 million recorded the previous year. The service has been growing month by month since April 2024, when it was just R$150 million, according to data from the Central Bank (BC).”

🇲🇽 Belvo and JP Morgan Partner to Enhance Recurring Payments in Mexico - 👉Finovate

“Now a member of the J.P. Morgan Payments Partner Network, Belvo will enable companies in sectors such as lending, insurance, utilities, subscription services, and more to automate their recurring collections. By leveraging direct debit, these companies will reduce errors, ensure timely payments, and increase convenience for customers who will no longer need to make manual payments”

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.