#100: The revolution of instant payment systems in Asia and Latin America

W FINTECHS NEWSLETTER #100: 25/03-01/04

This edition is sponsored by

Iniciador enables Regulated Institutions and Fintechs in Open Finance, with a whitelabel SaaS technology platform that reduces their technological and regulatory burden:

Real-time Financial Data

Payment Initiation

Issuer Authorization Server (Compliance Phase 3)

We are a Top 5 Payment Initiator (ITP) in Brazil in terms of transaction volume.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

🍿 Too Long, Didn’t Read

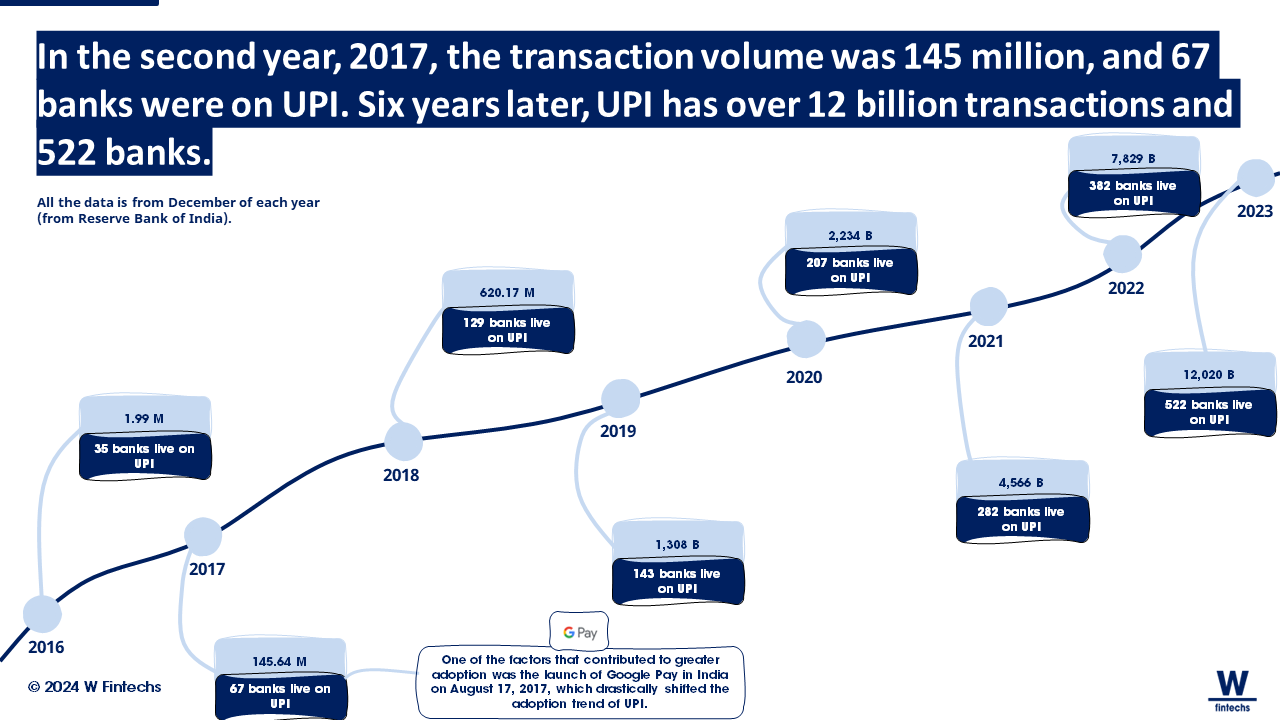

Just as the railway transformed the Indian economy, India has stood out for the digitalization of its economy. The major transformation came with digital identity, Aadhaar, in 2009, which provided identity to 1.38 billion residents and has already facilitated 102 billion electronic authentications; it has also saved the public coffers $33 billion. This paved the way for UPI, the instant payment system, which surpassed 20 billion transactions in 2023.

Another country in the Asian market that has excelled in terms of digital payments is Thailand, with PromptPay. PromptPay has helped Thailand achieve significant gains in digital and financial inclusion. The interoperability of the technology allowed the country to integrate its system with neighboring countries, enabling cross-border transactions.

The key lessons we can take from the Asian experience are that cooperation between industry and regulators and long-term vision impact the technology choices a country will adopt, consequently affecting adoption by the population. A simple and beneficial experience also aids adoption. Infrastructure costs pay off in the medium and long term.

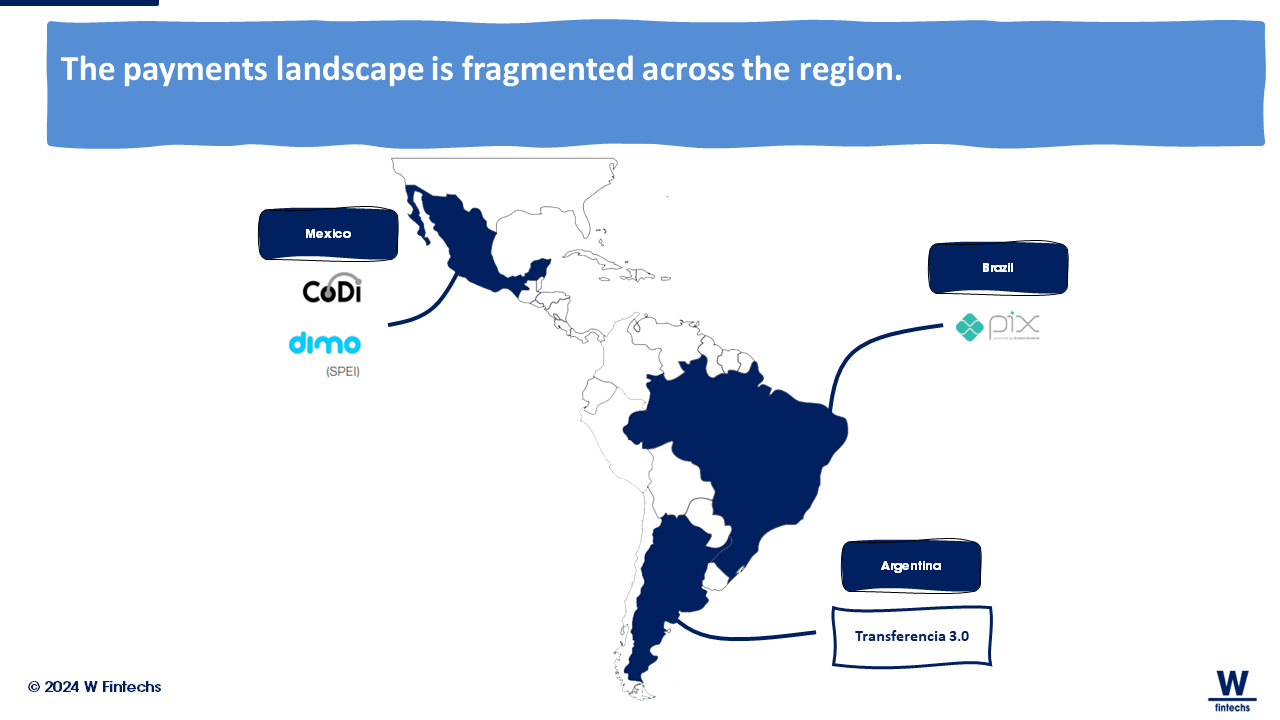

In Latin America, the scenario is more fragmented. Brazil stands out globally with the implementation of Pix, and with its evolution to Open Finance, however, Mexico did not reap good results from CoDi/DiMo, and also faced difficulties in implementing Open Finance. The causes of Pix's success are varied, but a regulator attentive to innovations and standardized messaging protocols and experience helped ensure Pix's success.

With the implementation of Open Finance and digital currencies, the fragmentation scenario can be diminished. However, in countries like Mexico, Colombia, and Brazil, there are a variety of approaches and challenges. While Mexico faces delays due to the lack of comprehensive secondary provisions from CNBV, Banxico moves forward with plans for third-party payment initiation in SPEI. In Colombia, although rules are being defined, the modernization of the payment system is slow. There are many lessons that can be drawn, such as the need to balance adoption incentives, such as fee exemptions, with long-term sustainability, and create an agenda that promotes network connectivity in each country. In Brazil, the regulator's proactive approach and solid technological infrastructure have resulted in rapid adoption of Pix and growth of Open Finance by consumers, companies, and financial institutions.

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

171 years ago, India's first passenger train departed from Bombay to Thane. During a 34 km journey, over 400 people boarded what marked the beginning of an infrastructural revolution that completely transformed the subcontinent.

With the establishment of the Great Indian Peninsula Railway (GIPR), it became possible to introduce railway services that revolutionized how people traveled and how trade operated in the country. The introduction of the railway system furthered India's economic development, and to this day, the country is recognized for having one of the most extensive railway networks in the world.

The Indian Experience

In 1853, India transformed its economy through the railway transportation; since 2010, the Indian government has been transforming the Indian economy into an integrated and connected one. The India Stack, the name given to the implemented technological infrastructure, has been reshaping the country's economy based on three pillars: (i) identity layer (with Aadhaar); (ii) Payment Layer (with UPI and RuPay); and (iii) Data Layer (with Sahamati). All these pillars, when interconnected, form the India Stack, which enables citizens, businesses, and the government itself to create new tools and interact through this platform.

The Pillar of Identity: Aadhaar

The creation of Aadhaar in 2009 is considered the game changer in India's digital history. Its primary objective was to promote innovation and include millions of Indians who lacked identity; subsequently, it aimed to build a digital ecosystem based on this foundation. The impact of this initiative is remarkable: Aadhaar has provided identity to 1.38 billion residents and has facilitated 102 billion electronic authentications; it has also saved the public exchequer $33 billion (as of October 2023)1.

The establishment of the Unique Identification Authority of India (UIDAI) in 2009 marked the beginning of laying a solid legal foundation. It was determined that UIDAI would be responsible for overseeing Aadhaar's development, collecting biometric and demographic data to assign a unique identification number to each citizen. The ecosystem created by UIDAI includes registries, update agencies, and authentication agencies based on public-private partnerships.

Aadhaar has been integrated into various government systems such as the Public Distribution System, National Health Mission, and Direct Benefit Transfer. These integrations have facilitated access to public services, reduced fraud, and improved the efficiency of government programs.

The Technology Behind Aadhaar

The technological architecture of Aadhaar was also crucial for the project's success. The project was developed based on principles such as openness, linear scalability, data security, and vendor neutrality. Aadhaar's technology includes biometric authentication, a 12-digit unique identification number, centralized storage in a data repository, and online authentication.

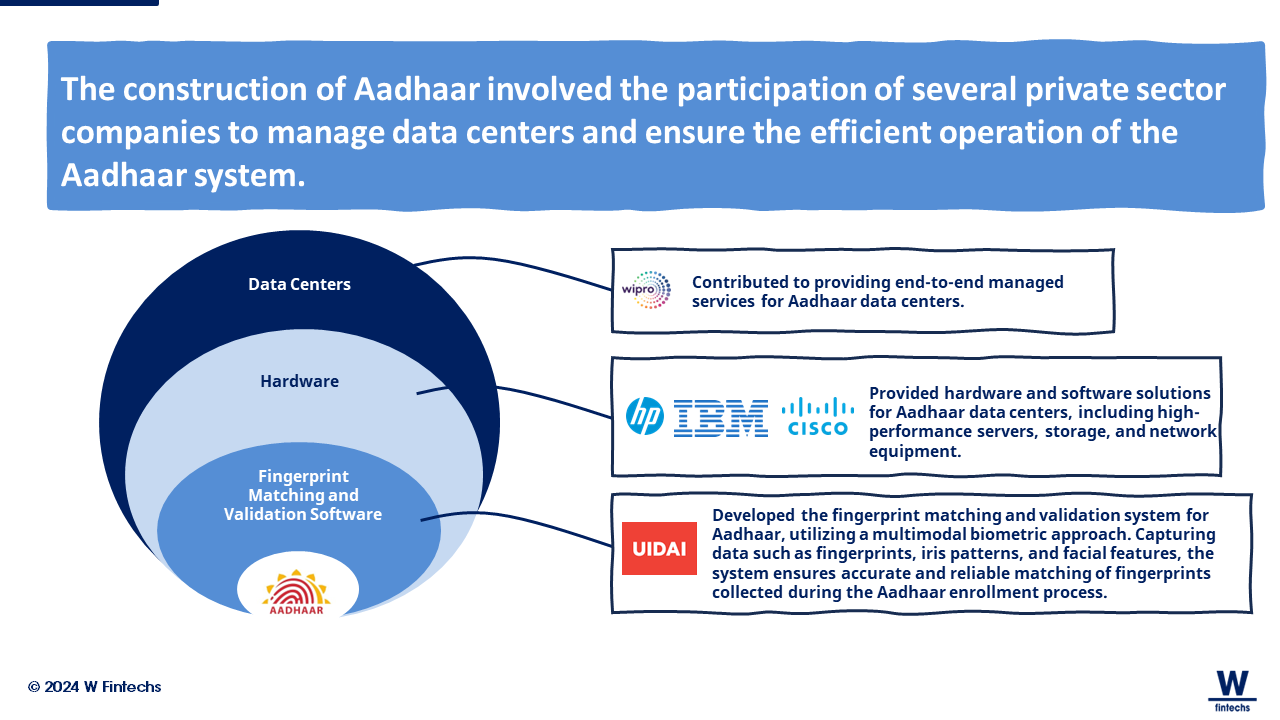

Aadhaar's data centers are managed by UIDAI itself and are located in various regions of India. The exact location of the data centers is not publicly disclosed for security reasons. However, it is known that the data centers are distributed across different states and regions of India to ensure redundancy and recovery capabilities in case of disasters. UIDAI has also implemented various measures to ensure the security and privacy of data stored in these data centers, including physical security measures, data encryption, and restricted access to the database. The project involved several private sector companies to manage the data centers and ensure the efficient operation of the Aadhaar system.

Companies such as Wipro, a consulting firm that collaborated with UIDAI to provide end-to-end managed services for Aadhaar data centers; HP, which provided hardware and software solutions for Aadhaar data centers, including high-performance servers, storage, and networking equipment; Cisco, which handled the security aspect and collaborated with UIDAI to provide network infrastructure and security solutions for Aadhaar data centers; and IBM, which offered hardware, software, and consulting services for Aadhaar data centers.

For the fingerprint matching and validation software in Aadhaar, UIDAI internally developed the Aadhaar Authentication Server (AUA) software. This system utilizes a multimodal biometric approach, capturing data such as fingerprints, iris patterns, and facial features to match and validate fingerprints collected during the Aadhaar enrollment process. Advanced algorithms compare this data with the Aadhaar database to authenticate the individual's identity. Additionally, UIDAI collaborated with various other private companies to develop fingerprint scanners integrated into the AUA system, ensuring accurate and reliable matching during the enrollment process.

Monetization of Aadhaar

Despite being a non-profit initiative, the government charges fees to businesses using Aadhaar for identity verification. Additionally, services such as eKYC and the Aadhaar Enabled Payment System are additional sources of revenue.

The Pillar of Payments: UPI

The role of Aadhaar was fundamental to the implementation of the Unified Payments Interface (UPI) in India—especially in terms of digitizing the economy. By integrating Aadhaar with UPI, the authentication process for financial transactions became more efficient, secure, and accessible. By integrating Aadhaar with the bank accounts of Indians, the government could, for instance, electronically transfer financial assistance to approximately 200 million beneficiaries during the pandemic.

India, with its large informal economy, managed to excel in the rapid adoption of real-time payments.

The Emergence of UPI

India already had a real-time payment infrastructure called IMPS (Immediate Payment Service) launched in 2010. However, with technological changes and the emergence of players such as Big Techs entering the payment market, the government created an API layer called the Unified Payment Interface (UPI), which enabled the integration of these new players and modernization of payments.

The focus on the evolution of the payment system by the Indian central bank over the years has led to the creation of an enabling peripheral ecosystem, followed by the launch of IMPS, leading to a vision for a "less cash" India through increased accessibility and a unified interface.

UPI, launched in 2016, emerged as a real-time funds transfer system that links multiple bank accounts in a single mobile application, promoting more interoperability.

The NPCI (National Payments Corporation of India) plays a central role as the owner and operator of the IMPS (Immediate Payment Service) and UPI (Unified Payments Interface) payment systems. While IMPS allows transactions through an agent network, UPI enables the participation of third-party app providers, facilitating the entry of fintechs and promoting interoperability.

The multiplicity of channels, including smartphones and simpler mobile phones, has expanded the reach of these systems. Transaction fees vary between banks and non-banking institutions (PPIs), with interventions from NPCI and the government to ensure accessibility and sustainability, similar to the approach adopted by Brazil with Pix.

NPCI not only operates the IMPS and UPI infrastructure but also plays a role in the clearing and settlement of interbank transactions, using the RBI's (Reserve Bank of India) RTGS (Real-Time Gross Settlement) system.

Additionally, the BHIM (Bharat Interface for Money) service, developed in collaboration with iSPIRT, serves as an interface to access UPI. The government aggressively marketed BHIM as India's national app, resulting in high demand from the population. As an increasing number of customers actively sought banks to request the BHIM app, many banks, initially resistant to adoption, were motivated to join UPI.

The Flow of UPI

The adoption of UPI was swift thanks to its simple flow for users. Naturally, users need to have a smartphone and a bank account with a financial institution associated with UPI. With over 500 member banks globally, users must ensure their mobile number is registered with the chosen bank. Access can be through various overlay services such as BHIM (government), GooglePay, Paytm, PhonePe, or MobiKwik.

The process typically involves selecting the language, verifying the mobile number via One-Time Password (OTP), creating an app access code, and choosing the bank to enable UPI payments. The most crucial step is setting up a UPI PIN, which involves entering specific account details, generating an OTP for verification, and creating the unique PIN. Once completed, the app will provide a UPI ID, which is akin to a Virtual Payment Address (VPA). This was essential for making transactions without directly accessing one's bank account, simplifying the payment process.

How the Technology Works

On the technology side, the operation of UPI can be divided into three layers: (i) the user layer, represented by the user interface (mobile app or web), where payment initiation and VPA creation occur, along with user-side security measures; (ii) the intermediary layer, responsible for VPA validation, transaction security, and forwarding messages to the relevant bank, performing mapping and routing requests between the user and bank backend layers; and (iii) the bank backend layer, which verifies balances, performs transaction compliance, authenticates user requests, and executes transactions using payment platforms like IMPS, sending confirmation back to the stack.

Additionally, UPI features daily transfer limits and user requirements, accessible to Indian citizens and non-residents in certain countries. Also noteworthy is UPI's multifactor security, abstracting between user and bank account, biometric authentication, and PIN usage for secure transactions. These aspects solidify the benefits of UPI, offering an additional layer of security and convenience in financial transactions.

India's experience has shown that aliases (keys such as phone numbers, emails, etc.) are extremely effective if they are simple, easy to remember, and convenient to generate, as we will see in Brazil's experience. Transaction fees for users depend on banks/PPIs, with interventions from NPCI and the government on issues such as the prohibition of surcharges for customers opting for UPI payments.

What I find most interesting about the Indian experience is that, much like Brazil's Pix, India utilized UPI as a platform, which means that beyond the UPI's initial launch, India continued to innovate and continuously enhance the system to support more use cases and improve the features of existing use cases over the years to ensure the sustainability of the system.

The Thai experience

In Thailand, the objective was also similar to that of India. In 2016, the government launched Thailand 4.0, a program aimed at boosting economic growth over the next two decades, with a focus on technology and innovation. Similar to what India did with India Stack, the plan included the development of the digital economy and the modernization of the financial sector, highlighting the launch of the National e-Payment Master Plan and, in particular, the PromptPay project.

The emergence of PromptPay

Launched on January 27, 2017, PromptPay allowed fund transfers between accounts using identifiers such as mobile phone numbers, citizen identification numbers (ID), or company tax identification numbers. Developed in collaboration between Thai banks and a third-party payment service provider, Vocalink, PromptPay is operated by National ITMX, overseeing its operation to ensure smooth operations.

Additionally, the Bank of Thailand regulates PromptPay, ensuring compliance with the country's financial standards and utilizing the bank's own RTGS system, BAHTNET, to settle interbank payment transactions that occur through PromptPay.

PromptPay only allows direct participation from banking institutions, while non-bank payment service providers connect indirectly to the system through sponsoring banks as sub-members.

Participating banks are required to pay a membership fee, consisting of a monthly variable fee and an interchange fee. The fee charged by direct participants to sub-member FIs is based on a bilateral agreement between the parties. User fees are regulated by the Bank of Thailand, although participants have the freedom to adjust these fees.

The internationalization of PromptPay

Included in the central bank's roadmap is the plan for international expansion, aiming to facilitate payments for tourists in neighboring countries. India has also been seeking to internationalize UPI, and some partnerships are already progressing, but in terms of stage, PromptPay is more advanced.

In recent years, the Monetary Authority of Singapore and the Bank of Thailand, along with banks from both countries, have begun integrating their systems, PayNow (Singapore) and PromptPay, so they could offer similar benefits for cross-border transfers. Both countries have been offering their payment services since 2017 and have built their systems to bring more interoperability, utilizing smartphones to facilitate fund transfers.

The pilot launch was in 2021, with payment and remittance services provided by pilot participants. In a future edition, I will explore further the difficulties and challenges of cross-border payments, but this Singapore-Thailand project is very interesting in technical terms.

In addition to legal and governance challenges, the biggest challenge for an infrastructure enabling cross-border payments is how it will be integrated into existing settlement and clearing systems, as well as standardizing messaging.

There are several lessons that both countries have drawn from this project 2, the top three being that: (i) it's necessary to consider the time required for the legal differences that both systems may present; (ii) constant and frequent engagement with key stakeholders and cooperation from both financial industries are necessary; and (iii) creating controlled environments that allow for extensive testing is crucial, as we are connecting two infrastructures from different countries.

Without a doubt, PromptPay is one of the great success stories of Asia. One of the things we can learn from the Asian market is that digitizing the economy, promoting innovations in the payment system, and creating a cooperative environment between regulators and industry can lead to fruitful outcomes in terms of financial inclusion and further increase the potential for economic growth. These initiatives can increase access to credit and foster the emergence of new businesses.

The Latin American Experience

Latin America has also made history in terms of digitizing payments and the economy in general. Looking at e-commerce numbers, one can perceive the advancements in digitization, especially after the pandemic period: 3 out of 4 people in the region have made online purchases 3. But even after this surge in growth, the e-commerce share of total retail in Latin America represents 10%.

In terms of adoption and construction of real-time payments (RTP), countries vary among themselves. I like to analyze the RTP market in Latin America from two perspectives: first, how the government/regulators cooperated in the creation and implementation, and what their role was; second, from the perspective of incentives and costs, both for the industry and society.

The Brazilian Pix Experience

In this regard, I believe Brazil has positively stood out in both aspects. Brazil's experience with instant payment systems predates Pix, going back to 2002 with the introduction of the SPB (Brazilian Payment System).

The Migration from Deferred Settlement to Real-Time

A payment system has various methods for settling payments. Until the 1980s, the most common method was deferred net settlement (DNS). Essentially, it involved accumulating payments throughout the day and offsetting obligations in the central bank's books at the end of the day or the following morning. While this method reduced the amount of money in circulation, it also introduced settlement risk, especially if a bank defaulted, triggering a potential cascade of failures.

With the increase in wholesale payment values in the 1980s, central banks recognized the need to address this systemic risk. Guided by the Bank for International Settlements (BIS), many migrated to real-time gross settlement (RTGS) systems, where payments are settled immediately on a one-to-one basis. RTGS adoption gained momentum in the 1990s, becoming a requirement for joining the European Union. This shift eliminated settlement risk, as payments became final and irrevocable.

Brazil was one of the countries that, at the turn of the century, migrated to RTGS for wholesale operations and later extended it to retail operations as well, giving rise to the SPB in 2002.

The Journey to Pix

In 2016, the Central Bank of Brazil (BCB) began studying new ways to further modernize the payment system. Since 2013, Brazil has been discussing ways to bring more competitiveness to the payment market. If you go to any neighboring country, you'll notice a strong concentration in the point-of-sale terminal market, usually led by Visa and Mastercard. Some establishments offer only one option, and there are also cases of charging an extra fee on the product. In Brazil, this scenario has been repeatedly addressed by the BCB.

Several measures taken by the BCB paved the way for the emergence of fintechs and greater competition in this market. Pix was born with this intention as well — to modernize and bring competitiveness to payments.

There are several studies indicating that payments serve as the entry point for many people into the financial system4. It was no different with Pix, which included 71.5 million Brazilians5.

WhatsApp Pay and the Central Bank of Brazil

The experience of PromptPay and UPI brought valuable lessons to Brazil, with the main ones relating to the importance of a simple, standardized experience for users and the industry, the use of aliases, and, in the case of India's UPI, the importance of combating payment concentration among Big Players.

In 2020, the BCB blocked the implementation of WhatsApp Pay by Facebook. At that time, Pix had not yet been implemented, and according to the BCB, the tool "could cause irreparable damage to the Brazilian Payment System, notably in terms of competition, efficiency, and data privacy." In China, something similar to what the BCB feared occurred, where two players monopolized the payment sector, making interoperability difficult for others. In India, the same scenario unfolded, with PhonePe and Google Pay controlling 83% of payments.

The pursuit of interoperability and transparency guided the introduction of instant payment systems in Brazil.

The Pix Architecture

Pix saw rapid and significant adoption, with over 90% of active accounts linked to the system. This rapid diffusion can be attributed to the requirement imposed by the Central Bank of Brazil (BCB) on Payment Service Providers (PSPs) with over 500 thousand active accounts to join Pix.

The infrastructure of Pix, built and operated by the BCB, also contributed to its rapid growth. To function, the BCB created two entities, the Instant Payment System (SPI) and DICT (payment alias database). The SPI processes Pix transactions, ensuring their immediacy and security. Meanwhile, DICT allows users to use keys (CPF, phone number, email, etc.) to make payments without the need to provide bank details.

Additionally, the BCB utilized the National Financial System Network (RSFN) to support all operations, establishing instant payment accounts (Conta PI). Institutions with Conta PI are referred to as "direct participants" of Pix. Those who choose not to have these accounts or are excluded from having them are called "indirect participants" and must partner with a direct participant to make and receive Pix transactions.

The Conta PI is managed through the BCB's former LBTR system, known as the Reserve Transfer System (STR), which operates only on business days and during specific hours.

To ensure that Pix transactions occur smoothly, direct participants need to carefully manage cash flow in their Conta PI. This is especially important at night and on weekends when demand for instant transactions may be high and liquidity more limited. The Central Bank of Brazil offers a limited liquidity credit line to direct participants and allows other participants to offer similar services to participants.

However, the credit lines are linked to the SELIC infrastructure, which is also limited to business hours. This means that outside of this period, participants may have difficulty obtaining liquidity, even with available credit lines. To reduce the cost and risk of managing Conta PI, the BCB later introduced regulatory changes to establish a yield to be paid on overnight deposits in Conta PI. This encourages participants to maintain higher balances in their accounts, even outside of SELIC operating hours.

On the other hand, DICT was introduced as an alias base that allows recipients to link a key – their taxpayer identification number, phone number, email address, or a random UUID – to a single account so that payers can make payments using only this information. Each key is linked to a single account, ensuring that payments are directed correctly. It is essential for DICT to function correctly at all times because before the clearinghouse can act, the system needs to know which bank account is associated with the key used in the payment.

The National Financial System Network (RSFN) is the private network of the Brazilian Financial System that supports data exchange for all critical financial infrastructures in the country, including SPI and DICT. To connect to RSFN, institutions must contract a direct link with the private network, as well as possess a digital certificate that meets certain criteria.

For an institution to become part of Pix, it must undergo a process full of certifications and technical validations. For the initial adoption by institutions, the BCB created a sandbox environment where aspiring Pix participants can implement their internal systems in a test environment, facilitating the implementation process. Once completed, new participants must take an additional step: undergo a series of technical tests to ensure that the implementation works with the BCB's systems and that payments can be successfully made, received, or initiated. This reduces the risks of compatibility issues in production, which can undermine the Pix experience.

The Technology behind Pix

The Central Bank of Brazil prioritized the development of fast, cost-effective, and easily integrable technology for Pix. The choice of open protocols and standards was crucial to achieving these objectives, as it ensured interoperability with other payment systems.

The implementation of Pix initially faced challenges related to the diverse landscape of the Brazilian banking system, where many banks have legacy technology. This is a constant challenge for implementing new technologies, and the BCB overcame these obstacles by creating a sandbox environment for testing, as mentioned above, and defining Service Level Agreements to ensure API quality.

Open protocols and standards played a significant role in Pix because they are cheaper options than available alternatives while being widely used and familiar to most technology teams. Additionally, since the initial goal of the BCB was to create an evolutionary agenda for Pix, these types of protocols are easier to extend for specific use cases. Instead of opting for IBM MQ, licensed by IBM, the BCB chose to use the HTTP protocol, which is free. These decisions had a direct impact on the final platform price, integration cost for PSPs, potential platform functionality, and implementation time.

The choice of the ISO 20022 format for messaging protocols aimed at interoperability with rails that share the same message format. However, for payments, ensuring interoperability goes beyond data format, requiring clear definitions on authentication, authorization, connectivity, and data requirements before the data format influences interoperability.

In a study conducted by Labrys, it was highlighted that the adoption of the EMVco QR Code standard in Pix presented substantial challenges and did not bring interoperability gains. The specific problem mentioned by the authors relates to "IDs 26 to 51," which are identifiers used within the EMVco QR Code standard. These IDs are assigned to different data sets, but the mapping between them is inconsistent and incompatible across various payment infrastructures worldwide. This creates difficulties in interpreting and uniformly processing these identifiers, compromising interoperability between systems.

Furthermore, the EMVco QR Code format imposes significant limitations. An example is the requirement to encode information, such as the merchant's name, directly into the QR Code. In Pix, this approach is considered inadequate as Pix relies on information from the DICT (Directory of Transactional Account Identifiers) to ensure data consistency.

Another limitation mentioned is the data field restricted to 99 characters in the Pix QR Code. In Pix, Uniform Resource Identifiers (URIs) are used to represent payment information. The 99-character limitation in the Pix QR Code makes it difficult to include extensive payload URIs, hindering more complex transactions. With more space, PSPs would have the flexibility to include all information directly in the URI, streamlining the payment process and reducing additional interactions with the beneficiary.

Pix was the result of a joint effort between regulators and the industry. As observed in Asian experiences, Pix relied on a centralized clearinghouse, responsible for processing and recording all transactions, and the inclusion of indirect participation allowed smaller institutions to participate in Pix, facilitating access to the system, its network effect, and reducing costs for participants — PSPs pay nothing to send payments and around $0.0002 to receive Pix transactions6.

The new system also allowed the association of metadata with any transaction, meaning that additional information could be attached to each payment, such as customer data, purchase data, among others. This flexibility enabled the creation of new services and functionalities in the future, ensuring the system's ability to evolve.

In the rest of Latin America

The payment landscape, as mentioned earlier, is fragmented in the region. Colombia has been making progress in implementing a more modern and interoperable instant payment system. Chile also has a real-time settlement system but still lacks overlay services. Another country that has made progress in this regard but has encountered challenges along the way is Mexico.

The Mexican Experience with SPEI

SPEI (Sistema de Pagos Electrónicos Interbancarios) is Mexico's main payment system, developed internally by Banxico, enabling real-time electronic fund transfers. Launched in August 2004, it replaced the old real-time gross settlement system, SPEUA (Sistema de Pagos Electrónicos de Uso Estendido).

SPEI processes high-value payments for financial institutions and large corporations, as well as day-to-day payments for the general population. To further facilitate payments and collections, the Bank of Mexico launched an overlay service called CoDi (Cobro Digital) in September 2019, which operates through SPEI, available 24 hours a day, 7 days a week.

Initially, SPEI operated for 11.5 hours. From 2015, the hours were extended to 20 hours and later to 24 hours a day. As the Mexican central bank introduced technological improvements, transaction processing time in SPEI decreased from 30 to 5 seconds. For transactions via CoDi, the time was reduced to 1 second since March 2020.

SPEI allows transactions in both traditional and alternative delivery channels, although QR and NFC are supported only through the CoDi overlay service. There is a pricing scheme developed for participants aimed at covering all development, maintenance, and operation costs of SPEI. It is a combination of fixed and variable fees. Regarding participant charges to customers, the Bank of Mexico allows free pricing for sending payments.

All banks and non-bank financial entities regulated and supervised by the Bank of Mexico and other Mexican financial authorities are eligible to participate in SPEI. Access requirements are essentially the same for all participants considering the level of risk, ensuring equal treatment for entry into the system.

The SPEI Technology

As an older system, SPEI adopted a proprietary messaging standard designed and developed by the Banco de México itself. According to World Bank documents, the Banco de México considers its proprietary standard quite efficient and has no immediate plans to migrate to ISO 20022. Additionally, SPEI participants have also not expressed a desire to adopt any international standard 7. SPEI also has a hybrid settlement scheme (every 3 seconds or a configurable number of payment messages), using a multilateral netting algorithm executed in rapid successions to clear and settle transactions.

Betting on Overlay Services in Mexico

Despite SPEI being the primary system in Mexico, there are few transactions made through it. In 2021, SPEI processed a daily volume of transactions of approximately 11 million payment orders, without its capacity being fully utilized, according to data from the Mexican central bank. The launch of CoDi was an attempt to increase the number of transactions, but it was unsuccessful due to its poor user experience. In March 2023, the Mexican central bank then launched Dinero Móvil (DiMo), intending to offer a much easier-to-use experience than previous solutions.

Instead of complex bank codes, users only need the recipient's phone number to make instant transfers via SPEI. This change aims to boost adoption of the system, especially among small merchants and consumers who do not have bank accounts.

DiMo is not just an evolution but can be a game-changer for the Mexican payment system. The country's major financial institutions already recognize its potential and are actively promoting the service. For example, BBVA expects to onboard 5 million users in the first year and transact more than $560 million.

Banxico has also relaxed the rules for opening level 2 transactional accounts, which are easier and quicker to open than a traditional account as they require less documentation and verification requirements. The DiMo app also allows for the opening of bank accounts directly on the platform, something unprecedented in Latin America.

Fintech company Finsus, for example, offers onboarding in less than 10 minutes. Additionally, affordable fees are crucial for mass adoption. Currently, transfers are free, but banks may charge in the future.

Pixel or not to Pixel?

The experience in Asia and Latin America highlights that, despite challenging economies, it is possible to digitize the economy through far-reaching public or public-private initiatives. However, the challenge lies in how this entire new payment system will be built. In the table below, it is possible to notice that Asian and Latin American economies have differentiated in terms of approach. Some adopt their own messaging standards, while others use international standards. While governments seek interoperability among technologies and platforms, it is highly likely that we will see an update, perhaps gradual, in this regard in the coming years.

Another point that I see will be interesting to observe is how these payment systems will interact with new payment entities, such as payment initiators, as the implementation of Open Finance progresses in these countries. Some have built technologies that support APIs, while others have not adapted.

In Mexico, in terms of Open Finance implementation, the country has been lagging behind other Latin American countries, such as Brazil. The financial regulator responsible for this implementation, CNBV (National Banking and Securities Commission of Mexico), has not yet published secondary provisions covering transactional data. Responsible for issuing specific guidelines for data providers and requestors, CNBV has only issued guidelines for aggregated data. On the other hand, Banxico, the operator of the SPEI, has decided to move forward with plans for a regulatory framework and a platform for third-party payment initiation within the SPEI. Banxico has mentioned the intention to create a centralized API hub that will facilitate payment initiation through third-party apps and SPEI participants via a single API connection. In practice, third parties will connect to the platform, which will transmit the payment initiation request to the end-user account service provider (e.g., a bank), so that the bank can send the payment to the SPEI. This lack of "alignment" between regulators may, in practice, further fragment implementation and perhaps bring more challenges. This is one of the major challenges in Open Finance implementation when the country has different regulatory bodies. In Brazil, despite the country having three distinct regulators overseeing areas such as investments, insurance, and payments, the country has established good governance that has not posed significant challenges, so far, for the expansion of shared data.

In Colombia, financial regulators have been progressing with the disposition of participation and technology rules for Open Finance, but the modernization of the payment system is still in its infancy. I believe that each experience mentioned here offers interesting lessons. The fee exemption in UPI, CoDi, and Pix, for example, has boosted their adoption, but it may be unsustainable in the long run. The lack of internet connectivity and low digital literacy, especially in developing countries, also pose challenges to reaching the entire population. In Mexico, for instance, we can see that the regulator has eased the adoption process for the new overlay service, as the country has a large portion of the population without bank accounts and prefers cash. Meanwhile, India and Thailand invested in digitizing the economy before launching their instant payment systems.

In Brazil, the regulator's approach with the industry, making adoption mandatory, and the way the technological infrastructure was built, facilitated a network effect in adoption by consumers, businesses, and, in technological terms, by banks and fintechs.

Instant payments have the potential to revolutionize the economy of Latin America, bringing more competitiveness, simplicity, and financial inclusion. Despite the fragmented scenario in the region, probably with the advancements of other financial ecosystems in the region, such as Open Finance and digital currencies, we will see positive changes in the evolution of their RTPs.

Learn more at 📚

Lessons from Pix: How to build a real-time payments platform at its full potential 👈

Building Faster Better: A guide to inclusive instant payment systems 👈

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://www.indiastack.global/aadhaar/

The main challenges, the structure established, and some technical considerations are outlined in this material.

https://www.latitud.com/latam-tech-report-2023

In "Accelerating Digital Payments in Latin America and the Caribbean," the authors have demonstrated that digital payments play a significant role in financial inclusion. The research indicates that when people have access to digital payments, they serve as a gateway to other financial services, such as credit and insurance. People are more likely to use these services to save money, start or expand businesses, manage risks, and better withstand financial shocks.

According to the Pix Management Report, Pix has already promoted financial inclusion for approximately 71.5 million users who did not previously make bank transfers through TED (Transferência Eletrônica Disponível).

https://www.labrys.one/public/research-publication/lessons-from-pix

https://fastpayments.worldbank.org/sites/default/files/2021-09/World_Bank_FPS_Mexico_SPEI_Case_Study.pdf