#112: Short Takes: The Quest for Payment Interoperability in Southeast Asia

W FINTECHS NEWSLETTER #112: 05/08-11/08

👀 Portuguese Version 👉 here

This edition is sponsored by

Iniciador enables Regulated Institutions and Fintechs in Open Finance, with a white-label SaaS technology platform that reduces their technological and regulatory burden:

Real-time Financial Data

Payment Initiation

Issuer Authorization Server (Compliance Phase 3)

We are a Top 5 Payment Initiator (ITP) in Brazil in terms of transaction volume.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

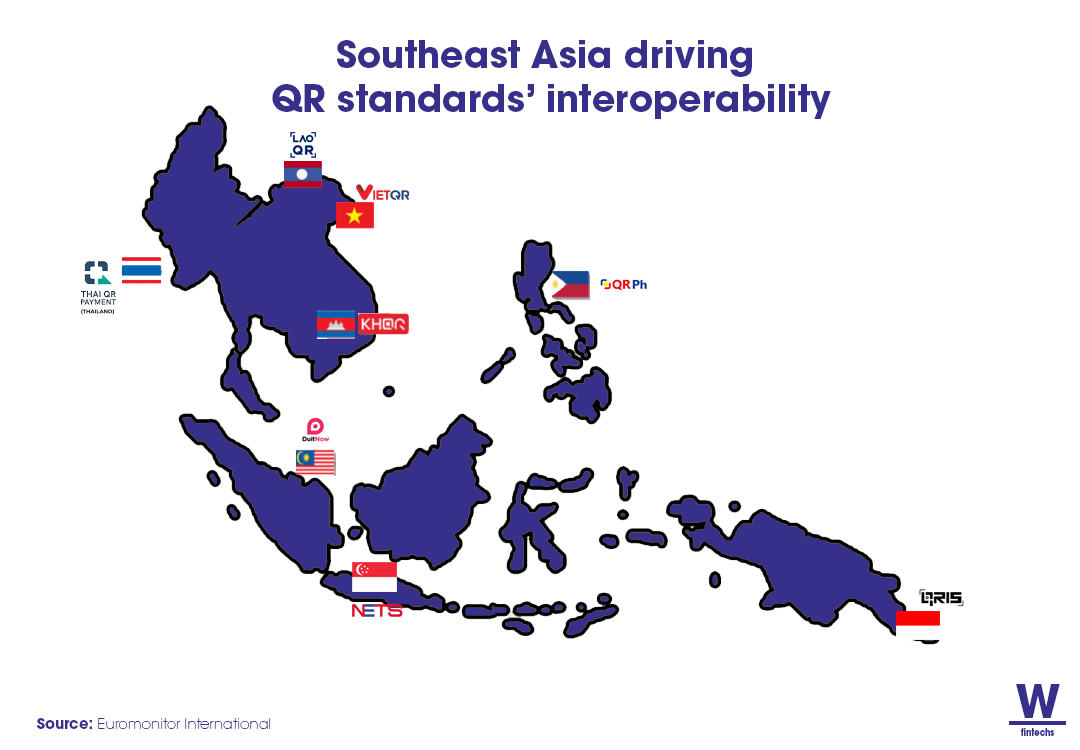

As more payment alternatives emerge, achieving interoperability becomes an increasingly significant challenge, particularly with cross-border QR codes.

Establishing interoperable systems is difficult, especially when dealing with legacy systems. This requires a solid and clear economic arrangement, well-defined technical characteristics, and governance capable of adjusting the course and reaching consensus on crucial decisions to avoid threats to the project's future.

In Southeast Asia, the evolution of payments has made the business environment increasingly competitive. Major players like Visa and Mastercard have collaborated with local banks in Thailand to introduce prepaid cards. Additionally, these companies have promoted contactless payments, aiming to replicate their successes in the Asia-Pacific markets.

Regarding cross-border payments, India 🇮🇳 has found success with UPI. Since February 2023, the Indian central bank has allowed foreign tourists from G20 countries to use UPI.

Similarly, PhonePe incorporated UPI International in February 2023, enabling Indian travelers to scan QR codes from merchants using PhonePe abroad and make payments via UPI in the local currency. This functionality is available even in destinations like Bhutan, Nepal, and Singapore.

Central banks in the region have played a crucial role in promoting this interoperability. Leading this progress are countries like Thailand 🇹🇭, Malaysia 🇲🇾, Singapore 🇸🇬, and Indonesia 🇮🇩, which have stood out by implementing a regional standard.

With increasing payment volumes driven by the growing participation of consumers and businesses both domestically and internationally, it's natural to expect a strengthening of interoperability between payment systems. In Latin America, countries like Colombia 🇨🇴 and Argentina 🇦🇷 are making progress in implementing a modern and interoperable payment system, and Brazil with Pix and Drex is making significant strides towards cross-border interoperable payments. As more nations adopt standardized and common messaging protocols, cross-border payments are likely to become even more straightforward and common.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.