#136: Short Takes: How did Méliuz reposition itself beyond the cashback market, aligning its strategy with giants like Klarna?

W FINTECHS NEWSLETTTER #136

👀 Portuguese Version 👉 here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Welcome to the Short Takes edition! As the name suggests, unlike deep dives, these editions will explore a variety of topics that might later evolve into full deep-dive editions.

Short Takes is designed for entrepreneurs, investors, and operators looking for quick, actionable insights.

💡 Want to advertise in the W Fintechs Newsletter?

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

Some businesses were born from an opportunity that, at the time, few saw or were delivering on. Over time, it becomes clear that those who stick to that one initial advantage end up falling behind. But those who build around that opportunity can stand out. Can — because there are no guarantees things will go as planned.

That’s the case of Méliuz, one of Brazil’s leading cashback players. The company went public in 2020, and although it was well-received at first, it later faced a series of losses in the following years.

Its initial bet on cashback paved the way for building a broader ecosystem — the boldest move being the acquisition of Banco Acesso, which brought Bankly into the mix, allowing Méliuz to offer Banking as a Service (BaaS) in 2021. It was an attempt to vertically integrate and enter the financial market as a digital bank. However, the strategy proved complex, and by 2023, Méliuz began the process of selling Bankly to Banco BV, its current partner.

In this edition of Short Takes, I’m not going to dive into Méliuz’s entire business journey, but rather into the transformation of the cashback market — a segment that has evolved from a promotional perk into a strategic tool in the relationship between brands, banks, fintechs, and consumers.

For a long time, cashback was seen as a bonus — a retail treat to encourage spending, typically tied to specific campaigns or loyalty programs. But that perception has radically changed. Today, cashback is at the core of strategies for banks, fintechs, and digital platforms — especially as a way to increase customer engagement and retention.

As e-commerce advanced, consumers became more benefits-driven and convenience-oriented, creating fertile ground for cashback to grow. Native cashback companies gained traction. Rakuten in Japan, ShopBack in Southeast Asia, TopCashback in the UK, and LetyShops in Eastern Europe all scaled their business models beyond just rewards. In Brazil, Méliuz was the most emblematic name in this wave.

But the landscape shifted. The entry of banks and fintechs raised the bar. Institutions like Nubank, Inter, and C6 began embedding cashback into the broader financial journey of their users. Cashback became part of the banking experience — available directly in the bank app, linked to the card, the digital account, and an array of financial products. It naturally became embedded into daily financial life.

In other words, what was once a differentiator became a commodity. And companies like Méliuz, which once dominated the space, had to choose between scaling at all costs or finding a new path to profitability. They chose the latter — but it wasn’t all smooth sailing.

Until 2021, Méliuz pursued aggressive growth. It made acquisitions, ventured into crypto, and tried to build out its own banking infrastructure. When it went public, many believed Méliuz was on track to become the next Banco Inter. But Brazil’s macroeconomic conditions and the high cost of those bets took their toll. The turning point came with the sale of Bankly to BV and a clear strategic pivot. Rather than becoming a bank, Méliuz chose to partner with banks and operate within a larger financial ecosystem.

That decision paid off. In 2024, Méliuz posted R$ 54 million in adjusted EBITDA, reversing a R$ 93 million loss from two years earlier. Net revenue grew, and its consolidated EBITDA margin jumped from -29% to +14.8%. The company traded disorganized ambition for purposeful efficiency in a more focused niche.

This new strategy also reshaped the product itself. Cashback stopped being the end goal and became the entry point for other services. With Méliuz Prime, the company introduced a recurring revenue model. With Méliuz Ads, it monetized traffic. And with BV, it built an asset-light operation to offer financial products at scale and with solid margins.

The number of cards issued in partnership with BV grew 4x in one year. The transaction volume surged by nearly 800%, and the user base reached 38 million. Personnel expenses were also reduced, falling by 32% in Q4 2024.

However, this operational maturity hasn’t eliminated all challenges. The market is saturated, and differentiation now needs to come from other areas: data, user experience, personalization. Méliuz understood this shift. It invested in improving its app and began to leverage the intelligence behind consumer behavior.

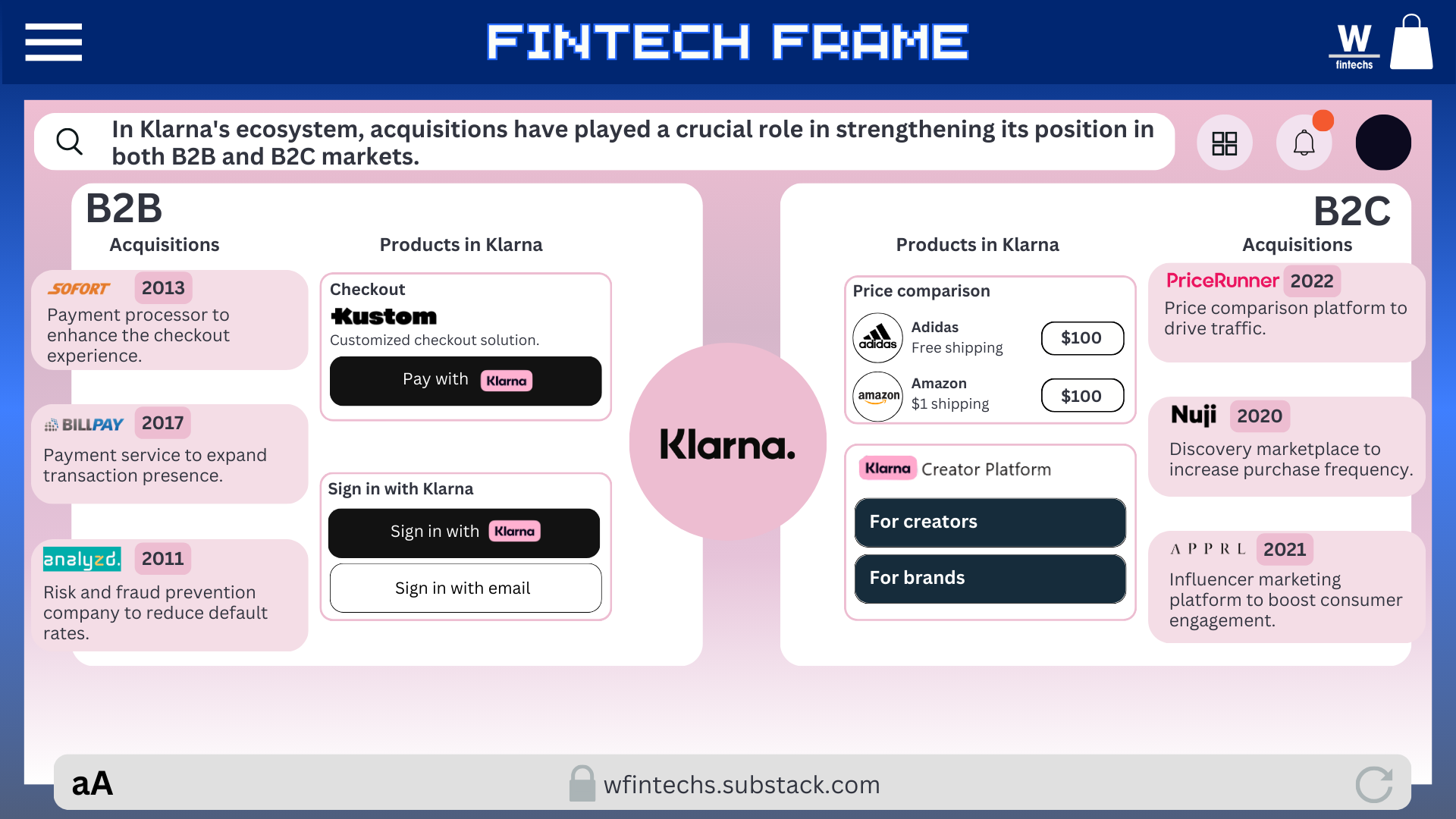

What Méliuz is doing is particularly interesting because it reflects a broader global trend. In edition #130, I highlighted how Klarna also sought to go beyond BNPL services and focus on operational efficiency — even integrating cashback into its U.S. offering, with rewards deposited directly into users’ accounts.

In Southeast Asia, ShopBack has evolved into a full-fledged benefits ecosystem, offering plugins, coupons, and partnerships with travel, delivery, and marketplace apps — building its value around its products and services.

It’s clear that players in this space today aren’t just competing for transactions, but for attention. For data. For loyalty. Cashback is just the starting point — retention is the real goal. Méliuz, Klarna, ShopBack, and other platforms that started with niche products have figured this out. They’ve built ecosystems that don’t just offer financial returns, but a sense of belonging, convenience, and intelligence.

Until the next!

Walter Pereira

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.