#FinOpen: 4 Years of Open Finance in Brazil; Use Cases; Updates

W FINTECHS NEWSLETTER #125

👀 Portuguese Version 👉 here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Welcome to this edition of the Finance is Open series.

Every other Wednesday, in addition to the regular Monday editions, I’ll cover the key topics and latest updates on what’s happening in Open Finance, both in Brazil and around the world.

Here’s what you’ll find:

A quick recap of the main developments from Open Finance Brazil’s working groups;

An analysis of Open Finance, whether in Brazil or globally, covering news, reports, or even personal insights on the topic;

And finally, an updated mapping of use cases.

Finance is Open is sponsored by

Iniciador is the complete infrastructure platform specialized in Regulated Open Finance, enabling Payment Initiation and Data Access.

The solution removes technology and compliance concerns, allowing clients — with their own regulatory license or using Iniciador’s — to focus on new products and business growth.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

About the Section:

In this section, I’ll explore the key updates from Open Finance Brazil’s working groups and structure.

I will usually divide it into four topics: governance, which will cover changes in rules, guidelines, and management structure; technology, bringing updates on infrastructure, APIs, security, and integration standards; user experience, highlighting improvements in usability and user journeys; and ITPs, where I’ll address updates on the list of regulated participants and topics related to the Payment Transaction Initiator (ITP).

From December 2024 to January 2025, we saw important definitions and progress in the structure. As the foundations of Open Finance become more consolidated, we are moving toward a definitive governance and management model.

For those who may not recall, in the new model, there will be an interdependence between voting rights and financial contributions, ensuring that institutions that contribute the most to the system have a proportional role in decision-making.

In the old model, there were six seats held by associations and one independent advisor. In the new model, effective as of January 1, 2025, the number of seats has increased to eight with the addition of two new associations—Zetta and INIT (the Association of Payment Transaction Initiators) — as well as a new independent advisor. FEBRABAN will now have two votes due to the interdependence between voting rights and funding.

The Definitive Structure had been under discussion since 2022, and now we have taken important steps toward its realization, with new appointments: Ana Carla Abrão has taken over as CEO of the definitive structure, while Bruno Diniz has been announced as the new independent advisor.

Regarding data sharing, in January, it was determined that it would become mandatory for large institutions, which could lead to greater user adoption and new use cases.

On the technology front, the Automatic Payments API has been updated to version 2.0.0, now requiring institutions to conduct retry tests. These tests aim to ensure that institutions can properly handle payment failures, such as network issues or insufficient funds. To meet the new requirements, institutions must achieve at least 50% compliance, meaning their systems must pass these tests in at least half of the evaluated scenarios.

The Variable Income API documentation has also been updated, now including new products such as FIAGRO and FII. On the user experience side, the Experience Guide has been revised to align user journeys with Open Finance Brazil, and new guidelines have been added to mitigate the impact of iOS 18 on the hybrid flow.

In the ITP space, PagSeguro, Muevy and Dock can now initiate transactions within Open Finance, while corporate institutions (PJ) may request an exemption from Automatic Pix certification if they do not offer personal accounts.

In the 3-year Open Finance report, I wrote that in the jungle of Open Finance, the game is cooperative. And that remains true: beyond the competition among banks for user consent and for offering the most attractive financial products and services, the Open Finance landscape in Brazil is indeed a jungle. Various players are offering everything from data analytics to full regulatory compliance platforms. While there is competition among them, each player’s presence is essential for the survival of the ecosystem as a whole.

🤳Download

Download the full report with Open Finance Brazil’s achievements and use cases from its first three years. 👇 (PT-BR)

Over the past four years, Open Finance has advanced beyond just numbers. User experience has improved, with changes to the user experience guide and the introduction of the Redirect-Free Journey. Regulations have also been adjusted to increase engagement and expand institutional coverage, which will certainly drive more competition and use cases.

At the start of its implementation, Open Finance Brazil was heavily based on the UK’s experience in an attempt to predict what would happen here. But we quickly adapted to local realities and needs, leading to changes such as adjustments to limits and consent duration rules.

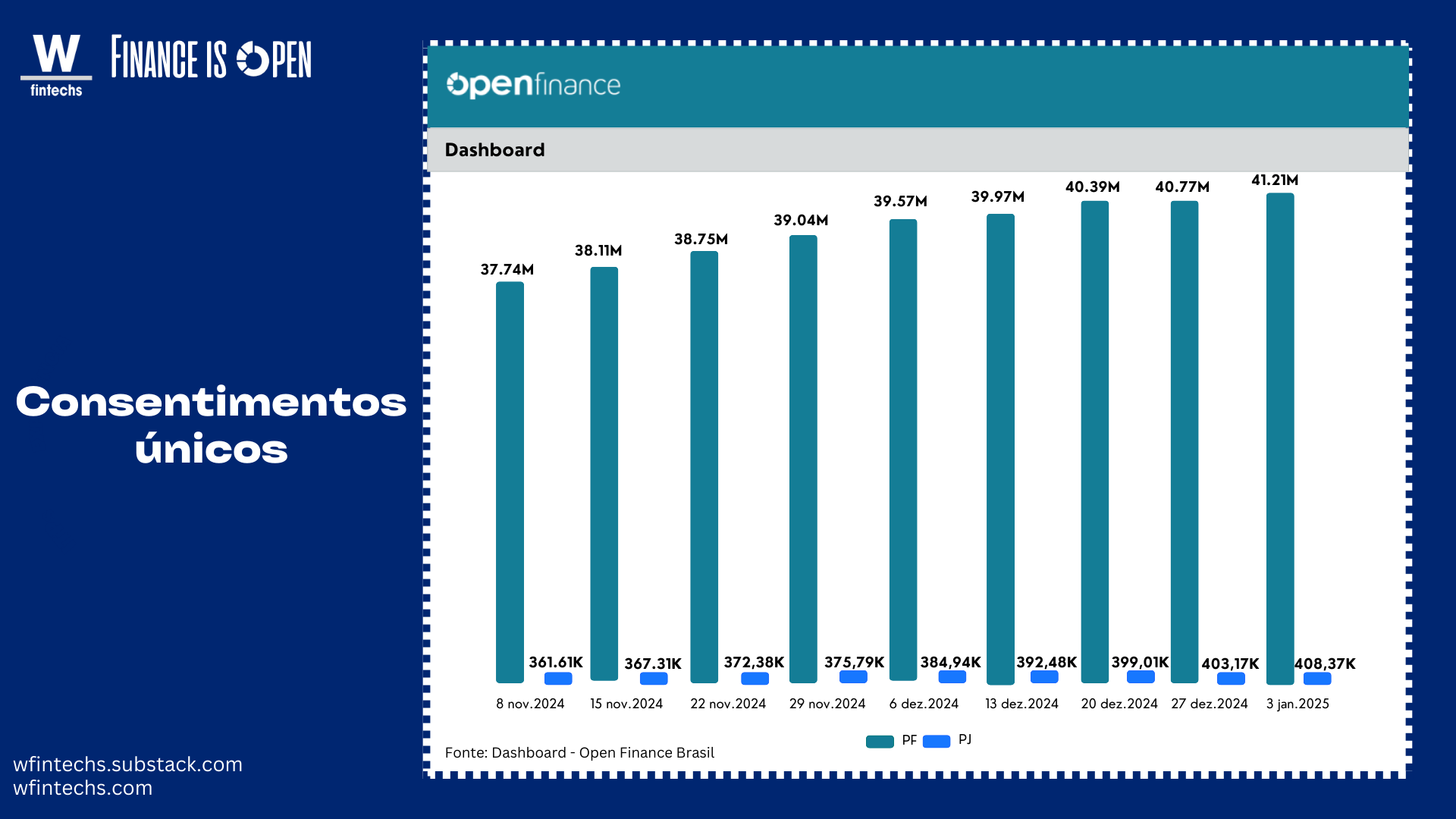

The numbers speak for themselves. Unique consents have reached 40 million, a 44% increase from 2023. Active consents have surpassed 60 million, growing by 48%.

Payment Initiators (ITPs), major banks, and fintechs continue competing for market share, and the data shows that new entrants are gaining traction, reaching a total of 50 ITPs.

Transactions have grown fivefold compared to 2023, moving R$3.2 billion. Meanwhile, payment methods remain the most effective way to drive recurring engagement, with Tap-to-Pay Pix being introduced as the next major milestone in embedding Open Finance into Brazilians’ daily lives.

After these four years, one thing is clear: Open Finance is moving beyond the adoption and implementation phase and into maturity. The challenge for institutions now is to capitalize on this moment to lead the next cycle of innovations and infrastructure expansion.

If you're enjoying this edition, share it with a friend. This will help spread the message and allow me to keep offering quality content for free.

Contribution

I'm creating a use case mapping, divided into data and payments, with an interactive dashboard. I’ve already mapped out some cases, but before the official launch (expected at the end of March), I want to enrich the mapping even further.

If you'd like to include your institution’s use case, just send me a message by replying to this email or via LinkedIn (link 👉 here). And if you're a fintech without its own license, don’t worry—we want you involved too!

Noh, which offers a digital joint account for couples, is leveraging Smart Pix to make transactions between accounts more seamless. With automatic and programmable payments, this solution eliminates friction and makes money management more intuitive, bringing a new level of convenience to users’ financial lives. Check out the flow in the video 👉 here.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.