#FinOpen: When a bank stops being just a bank and Open Finance becomes essential

W FINTECHS NEWSLETTER #159

👀 Portuguese Version 👉 here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Welcome to the edition of the Finance is Open series.

Every other Wednesday, in addition to the traditional Monday editions, I will cover key topics and the latest updates on what's happening in Open Finance, both in Brazil and around the world.

Finance is Open is sponsored by

Iniciador is the complete infrastructure platform specialized in Regulated Open Finance, enabling Payment Initiation and Data Access.

The solution removes technology and compliance concerns, allowing clients — with their own regulatory license or using Iniciador’s — to focus on new products and business growth.

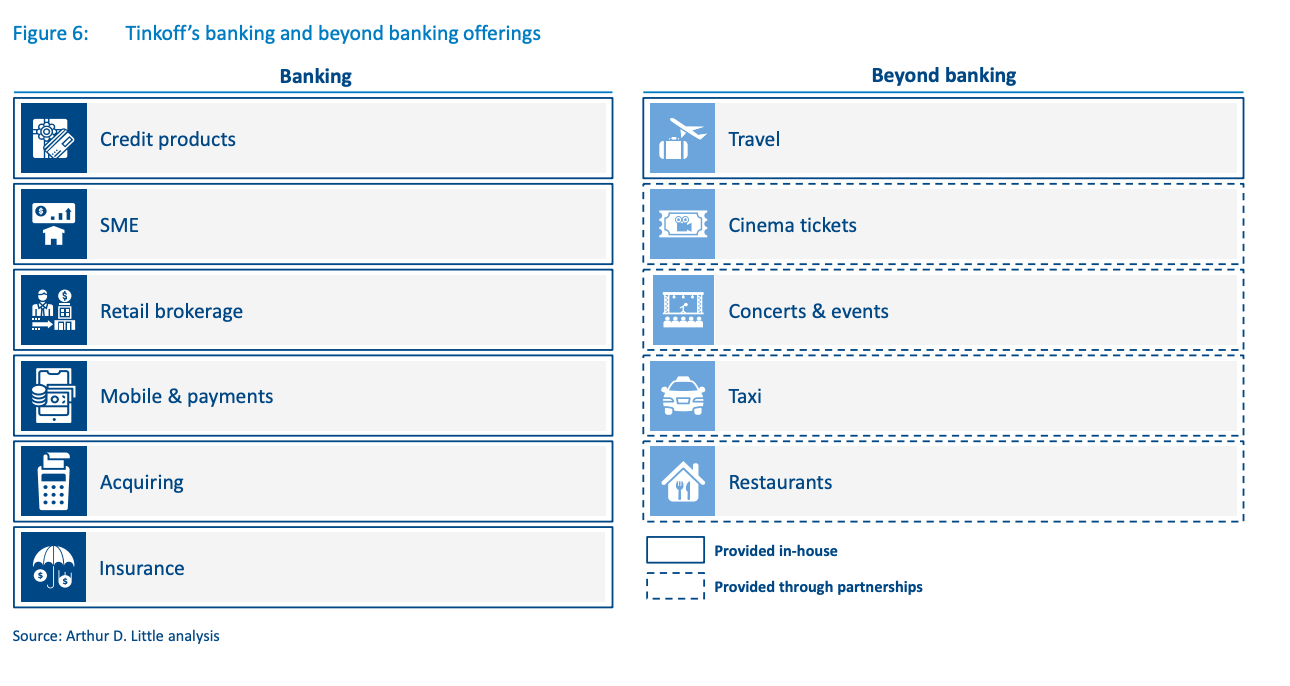

Seeing beyond banking merely as a bank’s entry into new sectors oversimplifies the complexity of what is happening. In the past, many institutions viewed this move as a way to increase revenue diversification or expand cross-selling opportunities. Gradually, however, the line separating sectors began to disappear, giving way to complete ecosystems that bring together different offerings. In this new scenario, financial services are no longer the goal but the means that support other user interactions.

In other words, this shift goes deeper than the idea of “offering other products” because it reorganizes the logic of customer acquisition and retention. In edition #133 of W Fintechs, I used the example of Nubank entering the telecommunications market as an MVNO to illustrate that the role reversal, where a fintech begins offering telecom services rather than the other way around, marks one of the many inflection points we have been experiencing in the banking sector in recent years.

It is no longer simply about adding a new product to the portfolio. It is about redefining the institution’s role in people’s lives, creating different touchpoints compared to the traditional banking relationship. These new spaces for interaction have the potential to generate more data, increase recurrence, and strengthen loyalty in a much broader way than financial transactions alone could achieve.

Looking at other markets, we see that the push toward beyond banking usually comes from three forces: saturation of the banking core, changes in consumer behavior, and regulatory advances that lower barriers to data integration.

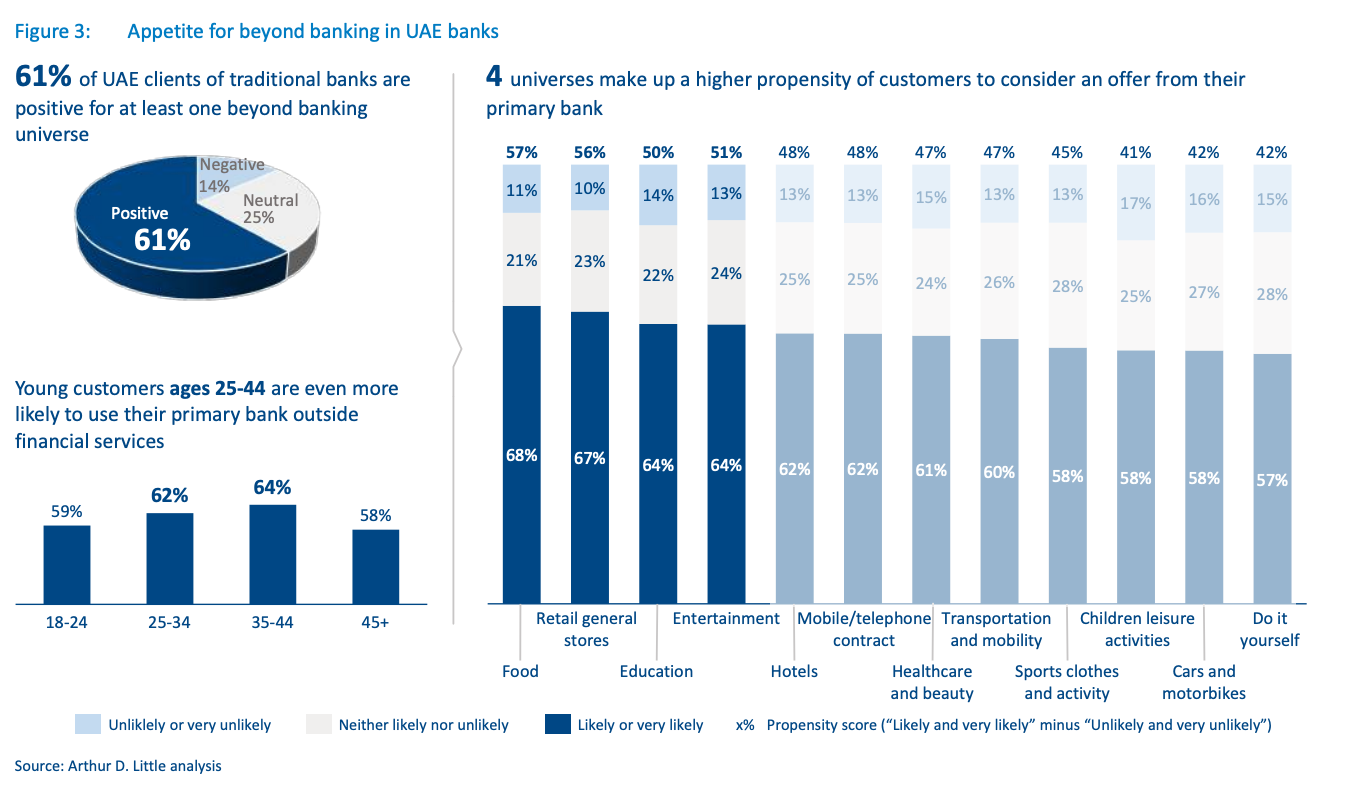

In the United Arab Emirates, 61% of bank customers would be willing to consume non-financial services from their own bank, with sectors such as education, healthcare, mobility, and retail leading this willingness 1. What is interesting about this figure is that it comes from a high-income-per-capita market, where the pressure to seek new revenue streams does not come from the base of the pyramid but from consumers who already have access to multiple providers and expect centralized and convenient experiences.

In Brazil, the regulatory and infrastructure vector is even more decisive. Brazilian Open Finance already brings together more than 55 million unique users, growing at a pace of 2 million new users per month, a speed seven times greater than that of the United Kingdom at the same stage. The entire framework created by the Central Bank has allowed, from the very beginning, the exchange of data across multiple financial segments, which has accelerated the ability to create beyond banking propositions. The fact that institutions access data from the same customer an average of 12 times a day indicates not only intensive usage but also the opportunity for the contextual insertion of offers for users2.

One aspect that is rarely discussed is how Open Finance redistributes competitive advantage. This means that even without a banking license, companies capable of orchestrating complete digital journeys can capture the primary relationship with the customer. In a scenario where financial services are entirely pluggable via APIs, customer loyalty can shift to whoever controls the experience, not necessarily to whoever holds the checking account. This opens up a huge space for what we can call the “distributed super app effect,” meaning that instead of a single dominant super app, we will have multiple hubs integrating finance invisibly.

This is where I believe instant payments become essential, precisely because they are the path to richer data, which can serve as a trigger for more bundled offers. Imagine a scenario where, upon paying for a ride-hailing trip, the system detects that the customer took more than 30 rides in the month and immediately offers a discounted subscription package, paid via instant debit and with cashback on fuel. This logic is already being tested in markets like India and Singapore, where the integration of instant payments with other services creates a transactional layer that acts as an engine for beyond banking.

In the SME segment, the gap is even more evident. A McKinsey study points out that small and medium-sized enterprises account for about 20% of global bank revenues but are underserved in terms of integrated digital services 3. Some players have begun to apply the beyond banking model to SMEs, combining different elements such as working capital, inventory management, electronic invoicing, and logistics integration into a single platform.

This logic has already been explored differently in African markets with mobile money. There, telecommunications companies turned financial services into a natural extension of their operations, leveraging the ubiquity of mobile phones. In other words, what we are now seeing with cases like Nubank and other Latin American players is the reverse route: fintechs entering adjacent sectors such as telecom or digital retail to expand the reach of customer relationships.

From a strategic standpoint, there are three possible roles for financial institutions in this scenario: orchestrator, partner, or specialist. The orchestrator controls the experience and integrates multiple services; the partner provides specific capabilities within larger ecosystems; the specialist offers a highly differentiated service that can be plugged into any ecosystem.

In practice, beyond banking also redefines the metrics for success. Instead of looking only at average balance or revenue per customer, institutions begin to track metrics such as interaction frequency, depth of engagement, and share of the customer’s total journey across different segments. In the long run, these metrics may become more accurate predictors of profitability and retention than traditional indicators.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://www.adlittle.com/sites/default/files/reports/arthur_d_little_reports_beyond_banking.pdf

EY - Open Finance Brazil Study, July 2025

https://www.mckinsey.com/~/media/mckinsey/industries/financial%20services/our%20insights/how%20banks%20can%20use%20ecosystems%20to%20win%20in%20the%20sme%20market/how-banks-can-use-ecosystems-to-win-in-the-sme-market-vf.pdf