#FinOpen: "Spotify of credit": a smarter personal loan powered by Open Finance

W FINTECHS NEWSLETTER #148

👀 Portuguese Version 👉 here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Welcome to the edition of the Finance is Open series.

Every other Wednesday, in addition to the traditional Monday editions, I will cover key topics and the latest updates on what's happening in Open Finance, both in Brazil and around the world.

Finance is Open is sponsored by

Iniciador is the complete infrastructure platform specialized in Regulated Open Finance, enabling Payment Initiation and Data Access.

The solution removes technology and compliance concerns, allowing clients — with their own regulatory license or using Iniciador’s — to focus on new products and business growth.

For a long time, personal credit was treated as a reactive product where the customer had to request it, justify their need, wait for analyses, and go through a slow, friction-filled process. With Open Finance, a new approach becomes possible: smart credit. Instead of waiting for the user to seek out credit, this model can anticipate their needs based on real-time data and remain continuously connected to their financial journey.

In recent years, some fintechs have attempted to build a sort of “Spotify of credit,” where the lending experience would be as fluid, predictive, and personalized as listening to music with all powered by alternative data and digital behavior. However, these initiatives ran into challenges such as lack of interoperability, scarcity of standardized data, and regulatory barriers. Now, with the advancement of Open Finance and growing competition between traditional institutions and new players, this hyper-personalized model is becoming more viable.

Imagine a scenario where your bank detects that one of your accounts is about to go into overdraft and automatically triggers a credit line from another institution or transfers funds from an account with a positive balance with all without the user needing to take any action. This concept takes shape in what’s being called the “global automatic overdraft line (or ”global overdraft”): a pre-approved credit line that covers shortfalls in any connected bank account. In other words, it replaces isolated products with a distributed layer of credit, seamlessly integrated into the user’s payment journey. By monitoring balances and upcoming transactions, this system can automatically reallocate funds, anticipating needs before problems arise.

This credit transition is already starting to show up in data from the Central Bank — as I highlighted in the previous edition of FinOpen. Since the beginning of Open Finance implementation in Brazil, over R$18 billion in credit operations based on shared data have been reported. Out of this total, fintechs have granted R$3.2 billion in credit to 4.3 million customers.

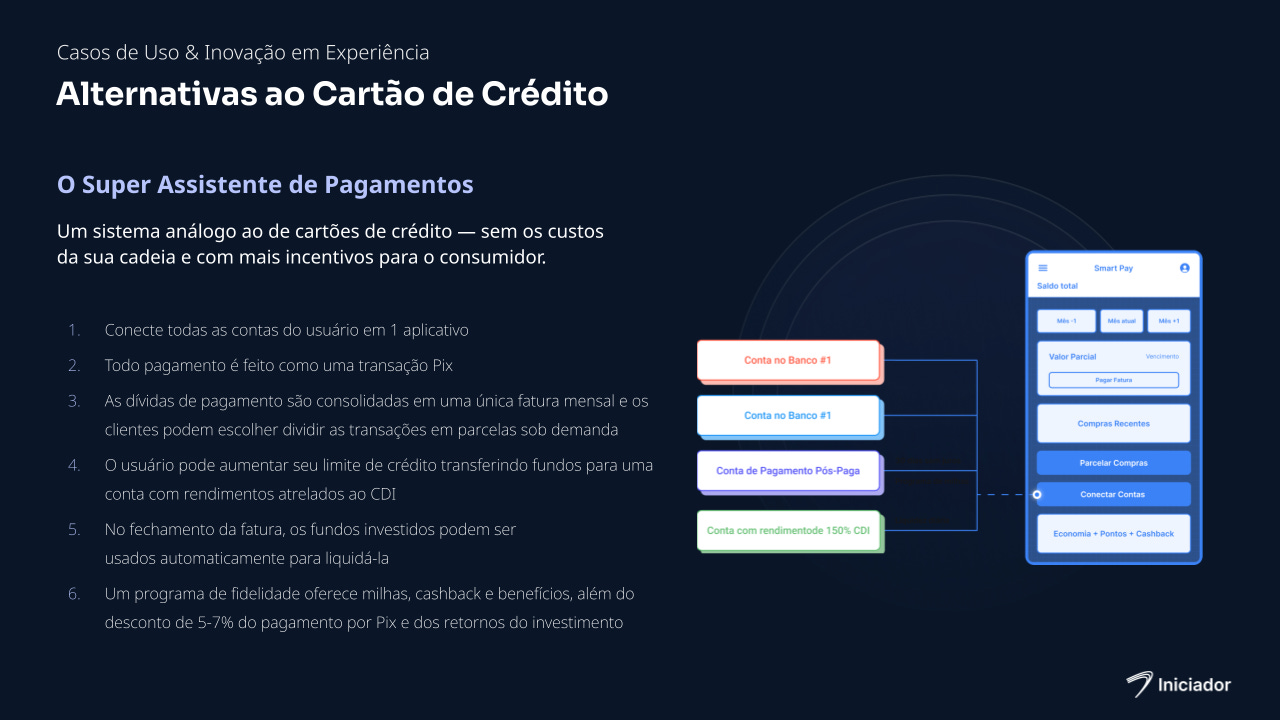

This logic ties into what’s being called the “Super Payment Assistant,” an alternative model to the traditional credit card. All of the user’s accounts are integrated into a single app. Each transaction is made via Pix, and monthly expenses are consolidated into a single bill with the option to split payments on demand. Meanwhile, funds can remain invested with earning returns, for example, at rates linked to the CDI (Interbank Deposit Certificate) and are only used at the time of payment.

This model can turn invested balances into an extension of the credit limit, and the returns into tangible benefits for the user — such as 5% to 7% discounts when paying the bill via Pix, for example. In this way, credit stops being a cost and becomes a service embedded within an automated financial management experience.

Products like Nubank’s "Parcela Compras" or Inter’s "Crédito na Hora" are moving in this direction, but still operate within closed ecosystems. The agnosticism and modularity enabled by Open Finance create space for new intermediaries to become credit channels.

ERPs, for example, can monitor a company’s cash flow and automatically trigger a receivables advance when a liquidity gap is detected. In 2024, nearly R$7 billion were transacted through solutions of this kind, featuring functionalities such as bank reconciliation and real-time quotes for working capital, according to a report released by the Central Bank in April. 1.

At the same time, the line between credit, payments, and investments is beginning to blur as Open Finance progresses. Invested funds can be automatically used to settle Pix transactions, and earnings accrue until the very last moment before a bill is due. This creates a new model of financial engagement where financial organization is truly rewarded, and credit operates as an invisible yet deeply integrated resource, closely tied to the user’s reality.

We may be getting closer to a “Spotify of credit,” where offers dynamically adapt to the user’s profile, and to a “Zapier of finance,” where accounts, balances, receivables, and investments connect in real time, automatically. In this new setup, the bank is no longer the final destination but acts as an orchestrator of data, financial products, and decisions. Smart credit then emerges as a natural outcome of this transformation — no longer an isolated product within the banking experience, but rather something embedded in a suite of solutions that genuinely improves the end user's financial life.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://www.bcb.gov.br/content/publicacoes/ref/202504/RELESTAB202504-refPub.pdf