#101: The pursuit of interoperability in Peru's payment systems and the future of digital wallets

W FINTECHS NEWSLETTER #101: 01/04-07/04

This edition is sponsored by

Iniciador enables Regulated Institutions and Fintechs in Open Finance, with a whitelabel SaaS technology platform that reduces their technological and regulatory burden:

Real-time Financial Data

Payment Initiation

Issuer Authorization Server (Compliance Phase 3)

We are a Top 5 Payment Initiator (ITP) in Brazil in terms of transaction volume.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

In the last edition, I wrote about how payment systems are being transformed into instant and more efficient ones in Latin America and Asia. Both regions stand out for their challenging economies and also for the high levels of adoption of their payment systems, albeit in a fragmented manner. India has been transformed by UPI, Thailand by PromptPay, Brazil by Pix — used by 80% of Brazilians, 13 million businesses, and 800 participating institutions — but in other Latin American countries, there are still challenges in adopting their systems. In Mexico, the regulator has sought to correct the course through overlay services. First, it was CoDi, now it's DiMo.

International experience, as I showed in the previous edition, teaches us that cooperation between the industry and the regulator, along with a clear long-term vision, impacts the technology choices a country will adopt, consequently affecting adoption by the population. A simple and beneficial experience also aids adoption, and infrastructure costs pay off in the medium and long term.

Another point that international experience teaches us is the need to combat the concentration of payments among Big Players.

In Brazil, for example, in 2020, the Central Bank of Brazil (BCB) blocked the implementation of WhatsApp Pay by Facebook. At the time, Brazil had not yet implemented Pix, and according to the BCB, the tool "could cause irreparable damage to the SPB (Brazilian Payment System), notably regarding competition, efficiency, and data privacy." In China, something similar to what the BCB feared happened, where two players monopolized the payment sector, making interoperability among others difficult. In India, the same thing occurred; PhonePe and Google Pay control 83% of payments. The pursuit of interoperability and transparency guided the introduction of instant payment systems in Brazil.

In Peru, the concern is the same. In a study published by the Central Bank of Peru in June 2023, the search for more interoperability to improve the payment experience was highlighted. Currently, the payment landscape in the country is challenging. The main payment method in Peru is cash. According to data from the central bank of the country, until 2022 cash usage accounted for over 90% of payments for goods or services. However, despite this preference, the use of online or mobile banking services has been increasing. The study acknowledged that this improvement was due to access to fiber optics, which has doubled in the last 5 years. Digital wallets have also gained relevance in Peru since the pandemic, with the number of operations conducted through digital wallets from September 2022 being almost triple those conducted in the same month of 2021. The Central Bank expects the implementation of interoperability to significantly increase these numbers.

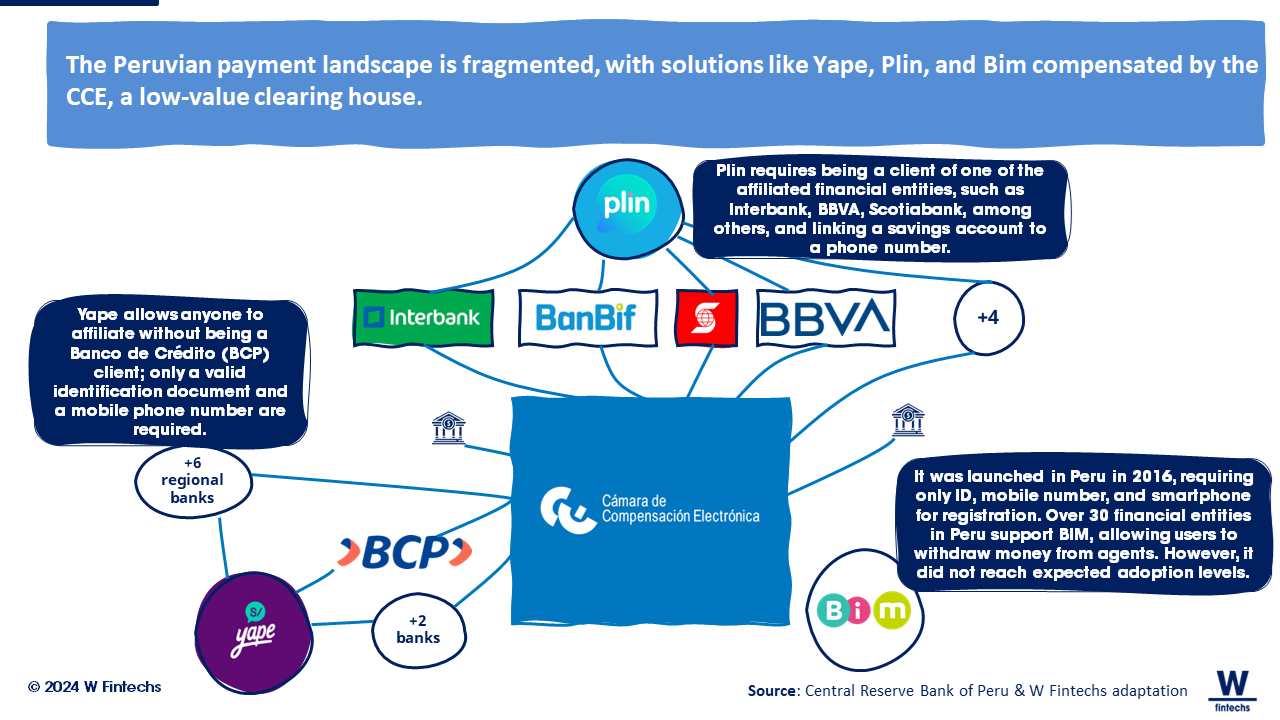

Despite this increase, Peruvians face a challenging user experience due to the proliferation of closed-loop solutions, such as Yape and Plin, operating in the card system, and BIM, an industry initiative that has not yet achieved the expected adoption. On the other hand, there is a regulated market compensation system for low-value transfers, represented by the Electronic Clearing House (CCE).

A standout player

Fintech Yape, created by Banco de Crédito del Perú (BCP), one of the largest banks in the country, has leveraged the country's setup to implement a growth strategy that caters to the specific needs of different groups, such as liquor store owners, taxi drivers, and ice cream vendors.

Yape has invested in increasing brand recognition in the country, aiming to establish itself as a payment solution. The main approach chosen has been the dissemination of its QR Codes. With Circular No. 024-202 from the Central Reserve Bank of Peru, which establishes rules for interoperability in various payment services, several players have also started adopting this in their products. Yape has integrated with different banks in its ecosystem and coordinated interoperability with other market participants.

Yape has adopted the strategy of becoming a super app in Peru, where digital payments are just one part of the functionalities offered. A similar movement was seen in Brazil with PicPay, which now has approximately 62 million users. PicPay, for instance, offers travel and health insurance products, investment tools, business management resources, and the option to purchase cryptocurrencies.

The growth of Yape is remarkable. By April 2023, the app had over 2.3 million registered microenterprises. The company's strategy involves providing all information to users, allowing them to decide to adopt Yape on their own, finding value in its use, and remaining loyal to the platform. Additionally, Yape plays a significant role in digitizing donations, facilitating support for non-governmental organizations and community groups.

For interoperability, there are various paths

Many countries have been pursuing interoperability both within and outside their borders. Technologies that can communicate with each other not only ensure greater access but also continuous evolution and consequently new use cases. Interoperability is essential for further democratizing the financial system and allowing customers to choose the best option. According to CGAP 1, interoperability is based on three factors: (i) a clear and fair governance model; (ii) economic arrangements that encourage the participation of all stakeholders; and (iii) secure and reliable operational models. In Brazil, we are witnessing a true transformation in the payment and financial data landscape, paved by Pix and Open Finance, respectively, thanks to the balance of these three factors. Pix, as I wrote in the last edition, was designed from the outset to be a true innovation platform, and since then, several new features have been created based on its infrastructure. In Open Finance, the standardization of APIs has enabled different banks to communicate with each other and ensured that customers can port their data to receive better offers.

In digital wallets, interoperability means the same thing: having the ability to select the electronic wallet that best suits your needs and exchange money without restrictions, based on individual preferences, not on social impositions. After Yape's announcement of the launch of a new product, Yape Empresa, which will include a fee for all transfers above S/25,000 per month (equivalent to 6000 USD), the scene in Peru became even more tense, further fueling the debate on monetization models and competition in the Peruvian financial market 2. While in the rest of the world, we can see more competitiveness in the digital wallet landscape, such as in the case of the US which has Venmo, Paypal, Cashapp, and Zelle; or in Brazil, where there is PicPay, PayPal, Google Pay, among others, with most of these options provided by third-party companies, not directly linked to banks. In Peru, the offering of financial apps is limited and all available options are offered by banks. It is believed that with more interoperability and a more competitive landscape brought by data-sharing infrastructures like Open Finance, more players will emerge, making it possible not only for data portability but also for consumers to choose the best option.

Recently, the Peruvian central bank published a new study highlighting the results achieved so far by interoperability in the country's payment system 3. According to the study, interoperability has improved competition and expanded access to new participants, driving the use and adoption of digital payments. By March 2024, Phase 1 recorded more than 2.5 million daily transactions, while Phases 2 and 3 are still under development. For Phase 4, a fair regulatory framework is being developed for the entry of companies such as fintech, bigtech e telcos into the interoperable ecosystem, already foreseeing payment initiation.

Despite the benefits that interoperability offers, there are several challenges to overcome. In addition to technical challenges, such as updating legacy technologies in banks; the choice of the implementation model to be adopted, whether the directory will be centralized, hybrid, or decentralized; and how the infrastructure will be financed. There are also structural challenges, very present in Latin American countries, such as low internet penetration, which reduces the population's literacy regarding digital and banking services, impacting adoption. Other countries, such as Colombia, are also reforming their payment systems, and it is very likely that in the very near future we will have even faster and more secure payments, with interoperability increasingly becoming commonplace, especially with Open Finance.

Learn more at 📚

The revolution of instant payment systems in Asia and Latin America 👈

Real Time Payments in Latin America and the Caribben: interoperability is the future 👈

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://larepublica.pe/opinion/2024/04/08/las-nuevas-comisiones-de-yape-empresa-y-open-banking-por-ragi-burhum-280816

https://www.bcrp.gob.pe/docs/Sistema-Pagos/articulos/estrategia-de-interoperabilidad-2024.pdf