#135: The super app strategy: turning a one-time customer into an ecosystem customer

W FINTECHS NEWSLETTER #135

👀 Portuguese Version 👉 here

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Before we dive into today’s edition, a quick note for those who joined last week — big welcome! Super glad to have you here. Every Monday, I share either a deep dive or short takes on financial innovation in Latin America. If you’re new here, here are three deep dive editions worth checking out:

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

As the competitive landscape intensifies — driven by new entrants and regulatory changes — players are being forced to rethink their strategies. In edition #123 (link 👉here), I wrote about how core banking is undergoing a transformation, especially with the rise of open-source technologies, as many players now seek greater flexibility over their ledger. Gaining control over the ledger has become essential to owning the revenue model, particularly in a context where some new regulations are eroding traditional revenue streams — such as the end of P2P transaction fees and caps on overdraft charges.

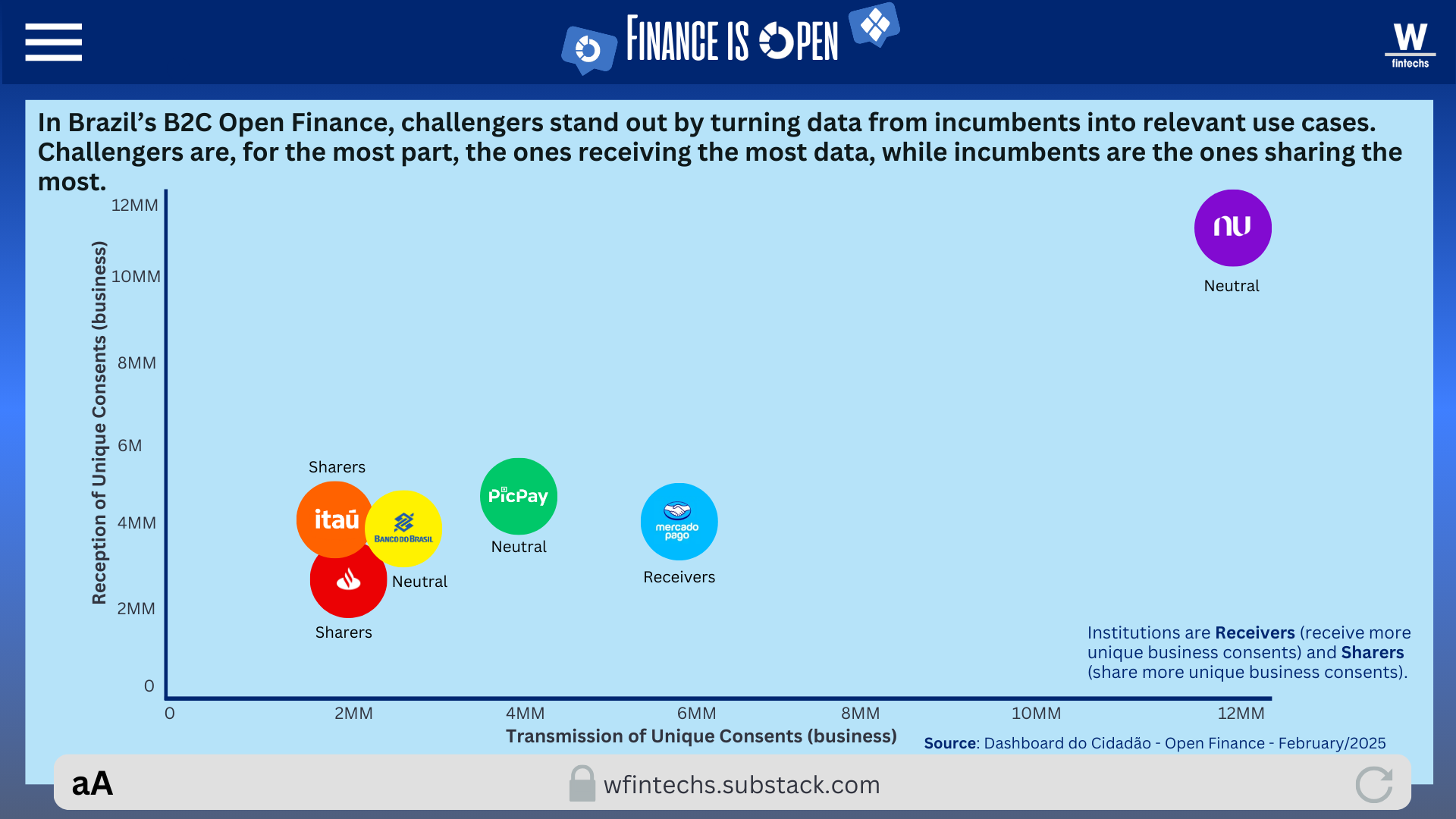

In other words, it’s time to look for new sources of revenue. Incumbents still hold an advantage that challengers are working to build: data. The idea is that the more data you have, the better you can anticipate your customer's behavior — at least in theory.

But data alone doesn’t solve everything. Among incumbents, some players are still in the early stages of becoming truly data-driven. In the context of Brazil’s B2C-focused Open Finance, it’s largely the challengers who are receiving the most data — while the incumbents are the ones sharing the most.

In the last edition of FinOpen (link 👉here), I highlighted how banks and fintechs are competing for territory in B2B Open Finance. While over 30% of the banked population already shares data under the B2C model, only 1.5% of businesses do the same. The strategies also differ — challengers are more active in the B2C space, while in B2B, players are testing different theses.

It makes sense that large banks would have a bigger appetite for B2B. Their quarterly results show that credit portfolios for this segment are more robust than those in B2C — BRL 461.1 billion at Banco do Brasil and BRL 662.2 billion at Itaú as of December 2024.

What I keep thinking is: if Nubank built a $50 billion business by focusing almost exclusively on B2C in its early days, it’s reasonable to assume there’s still a lot of untapped potential in B2B. The opportunities are there, but the challenges are different — more complex.

In today’s edition, I’ll explore how some players are expanding their reach in B2C to serve different moments in their customers’ lives. Nubank and Itaú are going head-to-head. Itaú, with the highest profits in the financial sector — over $6 billion — has decided to unify the digital experience in its main app by integrating its digital wallet, iti, into the bank’s core app. The focus now is to become a super app. It’s a move that seems to echo the path Nubank chose years ago — adding services and deepening customer relationships.

This move by Itaú and Nubank may very well be a smart way to increase average revenue per active user and customer lifetime value (LTV). But I don’t believe it’s the only path. Readers will quickly realize that with a super app strategy, the ambition is to become the central hub to a customer’s financial and digital life. Even so, when we look at the current level of integration, there are still many gaps to be filled.

How do super apps emerge?

When we look at the global distribution of super apps, it’s clear that this model first gained real traction in Asia and Eastern Europe — especially in emerging markets. That growth was fueled by a convergence of three key factors that supported the model at the time: unmet social needs, structural limitations common to developing countries, and technological advances that drastically reduced the cost of digital access.

The first generation of these companies reflected this reality. In regions with poor physical infrastructure and fragmented services, bundling multiple solutions into a single app wasn’t just convenient — it was a smart way to deal with scarcity and tight margins. Super apps became the main way to essential services: financial, logistical, social, and even governmental.

A central driver of super app development was mobile-first technology. Unlike countries where digital inclusion happened gradually via computers, in emerging markets the digital leap was straight to smartphones. With cheaper mobile and more affordable mobile data, it became possible to reach millions of people in record time. It’s no coincidence that in many African countries, mobile money was adopted by telecom providers as a way to leverage their network infrastructure to promote financial inclusion.

These multifunctional apps evolved from already-established services. WeChat, for example, began as a messaging app and later added payments, social networking, service bookings, and e-commerce. The key was frequency and relevance of user interaction. An app used several times a day for one specific purpose had a greater chance of expanding into other services — especially if it could remove friction in a simple, seamless way.

Another essential piece in building a super app was integration with the financial system. Adding payment solutions turned these apps into transaction platforms, which boosted user loyalty and deepened dependency on the ecosystem. Over time, these platforms started offering credit, insurance, investments — and eventually became full-fledged ecosystems.

The growth strategy behind super apps differs from that of traditional Silicon Valley apps. Rather than pursuing immediate vertical or global expansion, super apps grew horizontally, focusing on dominating their local market before diversifying their service portfolio.

Although super apps emerged in countries with generally unfavorable economic conditions, that variable actually contributed to their success. In developing nations, purchasing power tends to be relatively low — India, for instance, had a nominal GDP per capita of $2,099.60 in 2019, compared to $65,297.52 in the U.S. In this context, individual spending is limited, making it unlikely that a single service alone could generate enough return or sustain competitive advantage.