#FintechFrames: At the checkout of growth, Klarna leveraged data, card networks, and its positioning in B2B and B2C to redefine credit

W FINTECHS NEWSLETTER #130

👀 Portuguese Version 👉 here

Fintech Frames — Edition #01

Fintech Frames is a series by the W Fintechs Newsletter highlighting the journeys and strategies of fintech companies that have established themselves in the market — whether through an IPO, acquisition, or a valuation exceeding $10 billion.

For those looking for stories of founders still in the early stages, 3W in Fintechs dives into the beginnings of many ventures. Click 👉 here to explore all editions.

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

Building a strong B2C positioning is difficult. It requires significant capital, aggressive marketing investments, and a clear consumer benefit. Many companies fail before balancing CAC and LTV in their operations. Doing so while simultaneously building a solid B2B network is an even greater challenge. Klarna succeeded. By combining moves that include building a robust ecosystem, leveraging artificial intelligence to improve operational efficiency, and making strategic acquisitions, the company has helped redefine the shopping experience for millions of consumers in Europe and the US.

In 2021, I wrote that BNPL (buy now, pay later) was essentially a modern take on what Brazilians have long called crediário (click 👉here to read). The "buy now, pay later" model isn’t new. In Brazil, Samuel Klein built an empire with Casas Bahia's “crediário” back in the 1950s. Today, this practice has become a global trend, evolving with Open Banking, artificial intelligence, and the strategic use of data.

Klarna, along with Afterpay and Affirm, provided greater flexibility for consumers and higher conversion rates for retailers. Initially, many viewed BNPL as a threat to card networks. However, reality turned out differently. To scale, installment fintechs depend on the infrastructure of these networks. Visa and Mastercard not only endured but integrated BNPL into their systems. And it seems this will remain the reality as long as Open Banking payments are still in their infancy.

In this first edition of Fintech Frames, I'll explore Klarna's strategies and those of its competitors, delve into their financial metrics, and discuss the challenges BNPL faces in today's market. Readers will quickly see how the checkout has become a strategic space for e-commerce, where BNPL has successfully driven sales through behavioral science.

Sweden Was Too Small for Klarna

The story began in Sweden in 2005, when Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson noticed the e-commerce boom but realized payments still lacked flexibility for consumers.

Checkout has always been one of e-commerce's biggest hurdles, and today it's a battleground and opportunities. Solutions such as digital wallets, account-to-account payments, BNPL, credit and debit cards, and payment links all compete to offer faster, safer, and more convenient consumer experiences.

Looking back at the evolution of e-commerce, processes used to be more bureaucratic, registration forms longer, and intermediaries charged unclear fees, creating obstacles that harmed conversion rates. Each additional click increased the likelihood of consumers abandoning their purchase. The average cart abandonment rate in e-commerce is around 69.99%1, often due to payment flows that still require manual entry of card details and credentials.

Amazon quickly realized that reducing friction at checkout boosted sales, introducing features like the 1-Click Checkout, which allowed purchases with just a single click, eliminating the need to repeatedly enter payment and shipping information. It's no coincidence Klarna explored precisely this space.

Credit cards had high entry barriers and lacked payment flexibility. Klarna's initial idea was straightforward: allowing consumers to shop online and pay later.

The three founders didn't have a technical background, so Klarna's MVP was simple but effectively validated their initial hypothesis. They adapted an old concept to the digital world: customers bought online and received an invoice by mail 30 days later. The model worked, proving there was demand for BNPL from both consumers and retailers.

The company focused on a direct approach: customers made purchases, Klarna took on the risk, paid retailers upfront, and charged consumers afterward. While this seemed risky, the data favored Klarna: the consumer behavior was predictable.

Whereas banks structure credit first and then attract customers, Klarna uses BNPL as a customer acquisition tool, adjusting their analysis with each transaction. In other words, Klarna not only simplified transactions but leveraged their data to deeply understand consumer behavior. This allowed Klarna to rapidly scale, ultimately reaching millions of consumers and 500,000 retailers across 45 countries 2.

Different Strategies Over Time

To better understand the company's trajectory, I'll break it down into two main strategies. The first focused on checkout, when the three founders decided to improve retailers' conversion rates and offer consumers more flexible payment options. The second involved building an ecosystem extending beyond checkout, delivering direct benefits to both retailers and consumers.

The Checkout Strategy

The company's initial pitch to retailers was straightforward: increase conversions by up to 30%. For consumers, the appeal was simple: buy now, pay later.

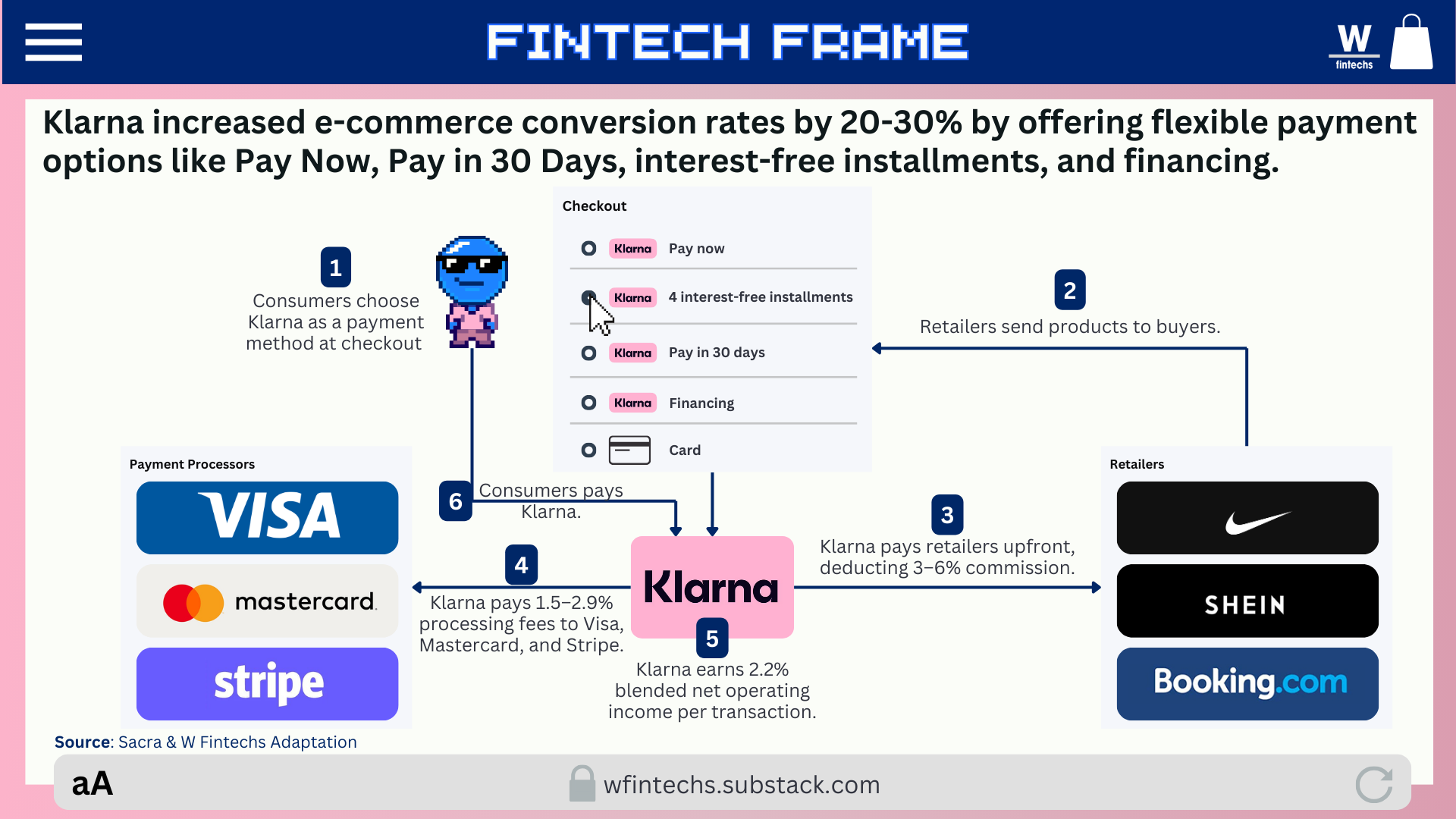

Product-market fit was achieved with Swedish e-commerce stores, which quickly embraced the "pay after delivery" model — allowing customers to receive their items first and pay afterward. The impact was immediate: conversion rates rose between 20% and 30%, and by 2010 Klarna was already processing 40% of all online payments in Sweden3.

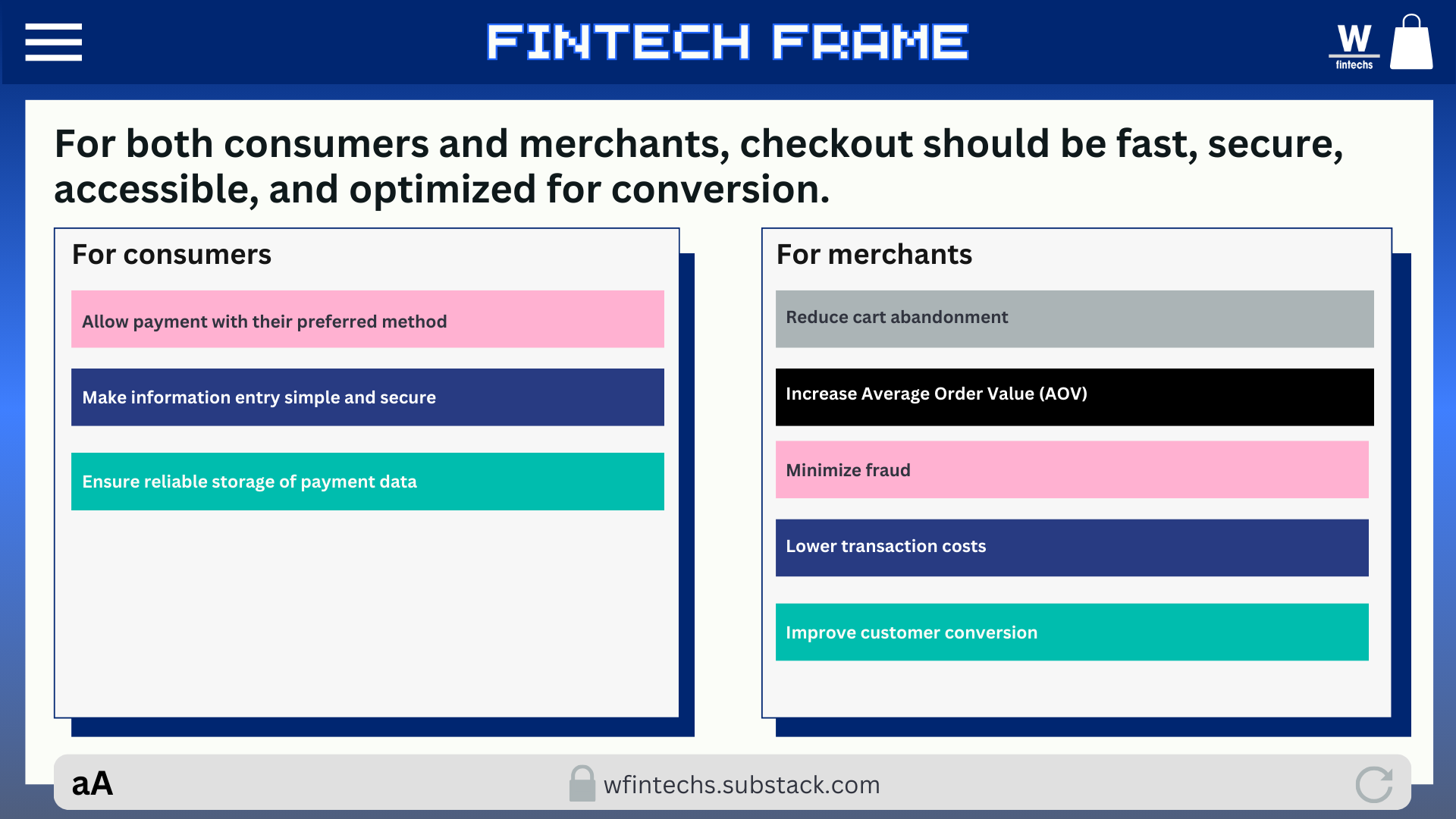

In the checkout process, multiple interests must coexist. Consumers want a quick, secure experience and favorable payment terms, while retailers aim to reduce cart abandonment, boost average transaction value, minimize fraud, and lower transaction costs. Successfully balancing these demands defines the effectiveness of a payment experience — and Klarna managed to do exactly that.

If previously payment options were limited — mostly restricted to immediate payments or within 30 days (such as with a credit card) — Klarna introduced more flexible alternatives, tailored to consumer needs. Now there's the option to "Pay Now" for those who prefer immediate settlement, "Pay in 30 Days" for those needing more time, split payments into three or four interest-free installments for smaller purchases, or financing between 6 to 36 months for those seeking longer terms.

Meanwhile, retailers receive the full purchase amount upfront (minus a fee between 3% and 6%). Consumers leave with their products, merchants get their money immediately, and Klarna assumes the transaction risk.

Klarna primarily generates revenue by charging payment processing fees ranging from 1.5% to 2.9%, plus an average operational spread of 2.2% per transaction.

An interesting point in this story is that the death of credit cards has been predicted for decades. In 2013, a Motley Fool article titled "The Slow Death of Credit Cards" spoke of an imminent collapse: between 2008 and 2012, total credit card debt decreased by about $200 billion, with banks writing off approximately $208 billion in bad debts. This resulted in a real reduction of per capita debt, reaching the lowest levels since 19964.

However, in practice, BNPL players like Klarna still depend on networks such as Visa and Mastercard to exist. These networks are essential for one critical reason: they process payments. Without them, most transactions simply wouldn't occur. Klarna and other competing fintechs, such as Affirm, utilize virtual cards — often issued by Visa and Mastercard themselves — to settle purchases with merchants.

The real question concerns the long-term scenario. Today, Klarna needs card networks to rapidly scale. While Visa and Mastercard are accepted by 170 million merchants, BNPL providers like Klarna and Affirm are still struggling to reach one million. Growth is impossible without infrastructure, and the quickest path was to partner with the already dominant system. Yet, this doesn't mean it will always be this way. Open Banking payments, although still in their early stages, offer an alternative route: direct account-to-account payments that eliminate intermediaries.

Card giants and banks themselves recognize this and have already launched their own BNPL solutions, aiming to maintain control. The traditional card model allowed banks to dominate consumer credit, but with BNPL fragmenting this market, Visa has repositioned itself to capture value regardless of who controls the transaction.

If BNPL is operated by banks, Visa continues providing infrastructure and settlement. If fintechs like Klarna and Affirm control the process, Visa steps in as the issuer of virtual cards and payment integrator. And if digital platforms like e-commerce and delivery embed installment options directly into their checkout processes, Visa fits in as the network layer supporting these transactions. Therefore, until Open Banking gains significant traction, the relevance of networks like Visa and Mastercard will remain intact.

The Ecosystem Strategy

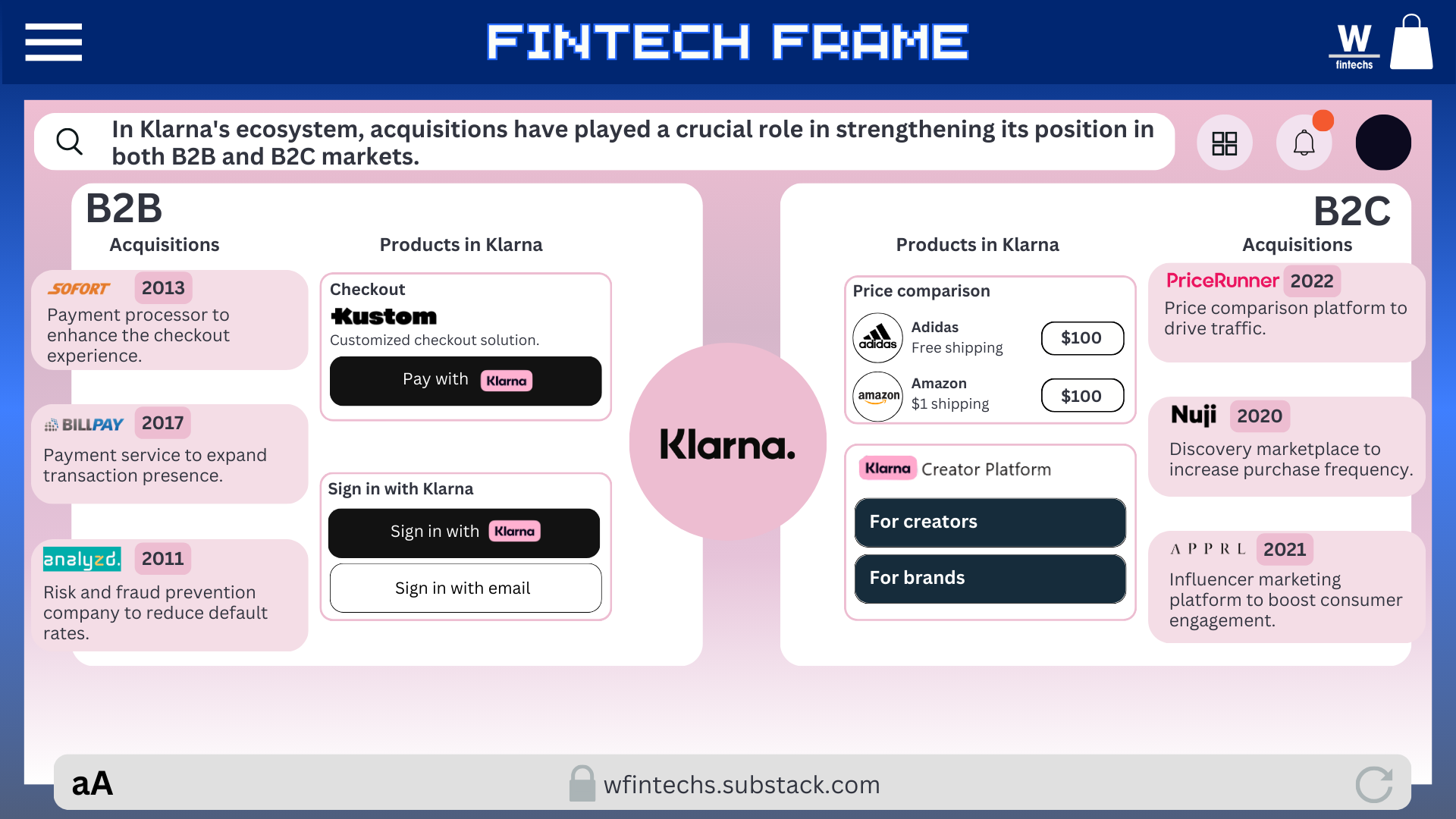

Simply being another button at checkout probably wouldn't have gotten Klarna to where it is today. Its competitive edge lies in creating an ecosystem connecting both B2B and B2C markets — a challenging endeavor. This ecosystem sets Klarna apart from networks like Visa and Mastercard, as well as traditional banks.

Card giants still control processing but lack direct relationships with consumers. Banks dominate credit but don't control the shopping experience. In contrast, Klarna not only facilitates payments but also helps consumers discover products via its superapp, closing the loop between consumer, retail, and credit.

Strategic acquisitions have been crucial for Klarna's expansion and ecosystem strengthening. In 2022, it acquired the price comparison platform PriceRunner, resulting in its own price comparison tool. This tool monitors thousands of sites in real-time to ensure the best prices. Many users come seeking discounts and end up discovering Klarna as a flexible payment option, becoming BNPL customers and increasing app engagement.

Other strategic acquisitions include Nuji, a discovery marketplace platform in 2020, and APPRL an influencer marketing platform, in 2021. These acquisitions helped drive traffic to Klarna’s platform and expanded retailers' reach.

From these acquisitions, Klarna developed the Creator Platform, connecting brands and influencers — a further strategy to facilitate transactions and deepen its involvement in the retail value chain, helping brands increase reach and conversions within an integrated ecosystem.

In the B2B segment, Klarna’s acquisition strategy focused on strengthening payment processing, notably through the purchases of analyzd, in 2011, Sofort in 2013 and BillPay in 2017.

It’s clear that Klarna isn't only competing for transactions but also aiming to control consumer desire and recurring. The higher the transaction volume, the greater its revenue, which boosts conversion rates and increases purchase frequency among retail partners.

If you're enjoying this edition, share it with a friend. This will help spread the message and allow me to keep offering quality content for free.

Klarna in Numbers: Growth and Strategic Shift Towards Efficiency

Despite these strategies, Klarna has experienced financial ups and downs over recent years. This is largely due to macroeconomic factors that frequently threaten business models like Klarna’s. This vulnerability became evident when central banks began raising interest rates throughout 2022, causing Klarna’s valuation to plummet from $46 billion to $6.7 billion during an $800 million funding round. This significantly impacted the company's strategic direction, prompting it to focus on greater operational efficiency. For this analysis, I’ll explore two reports: Klarna’s 2023 annual report and its September 2024 report, available directly from the company's website (link 👉here).

Although Klarna goes beyond just credit, risk management remains the primary challenge of the BNPL model. In 2023, the fintech reduced credit losses by 32%, driving down delinquencies to 0.38% of GMV. However, in 2024, this figure rose to 0.46% due to expansion in the U.S., a riskier market where consumers have different payment behaviors and greater credit exposure.

Nevertheless, Klarna has managed to maintain low financing costs and increase deposits from SEK 97.1 billion to SEK 106 billion over the same period, indicating the company can continue growing while burning less cash and buffering risks with deposits. This allows Klarna to leverage its own capital for growth instead of relying heavily on external loans.

Operational efficiency is evident in the numbers. In 2023, Klarna cut operational expenses by 16% and significantly reduced customer service and marketing costs. In 2024, over 90% of employees began using AI daily, enabling an additional 2% reduction in operating costs.

BNPL models are inherently sensitive to external factors, but Klarna's revenue strategy has supported sustainable growth across different economic scenarios. In the first nine months of 2024, revenue increased by 23%, driven by a notable 33% surge in the U.S. Unlike banks, which rely on interest income and struggle during economic fluctuations, 70% of Klarna’s 2023 revenue came from merchant fees, reducing its exposure to macroeconomic swings.

In 2023, Klarna achieved greater trust from consumers and retailers, reflected in a 22% revenue growth and a 17% increase in transaction volume on its platform. Klarna’s 2023 and 2024 performance shows the company intelligently adapting to a new global economic landscape.

Pioneering BNPL brought new competitors

In the evolution of BNPL providers, Klarna stood out as a digital pioneer, paving the way for new competitors. However, the increasing entry of major banks, card networks, and Big Tech companies has challenged its market position.

Previously, fintechs such as Klarna, Afterpay, and Affirm dominated the space, but now banks like CitiBank and Chase, card networks such as Visa and Mastercard, and Big Tech offerings like Apple Pay Later and PayPal Pay in 4 are major players.

For this analysis, I will focus on another fintech: Affirm. I believe Affirm's growth strategy is more comparable to Klarna’s, as unlike banks and Big Techs, both Klarna and Affirm had to build their user bases from scratch, covering both B2B and B2C markets.

Affirm

Founded in 2012, Affirm adopted a different approach. Half of its revenue comes from interest on loans, while the other half is generated through merchant fees. This balance positions Affirm between a digital lender and a payment platform. However, its heavy reliance on lending means its performance is directly tied to capital costs and consumer behavior.

The primary difference between Klarna and Affirm lies in their revenue structure. Klarna generates most of its revenue from transaction fees paid by merchants, operating more like a payment processor rather than a traditional financial institution — its main competitive advantage. Meanwhile, Affirm derives half of its revenue from loan interest, essentially functioning as a lender seeking profitability through maintaining customer balances.

This model has a direct impact on their finances. Klarna operates with short credit cycles, averaging around 40 days, allowing more efficient risk and default management. Affirm, on the other hand, faces greater risk management challenges precisely because it relies on longer-term loans, averaging around 11 months, acting more like a traditional lender that profits by maintaining open balances. This makes it more vulnerable to macroeconomic conditions and defaults.

👉 Subscribe to W Fintechs and receive an analysis like this in your inbox every Monday.

At the Checkout of Growth, Klarna Positioned Itself as an Ecosystem

The BNPL market was born from a clear proposition: increasing conversions for merchants and offering greater flexibility to consumers. Essentially, it's an evolution of installment credit, now adapted to the digital environment, with easier integrations and a simplified purchasing experience. What once required bank approvals and bureaucracy now happens instantly, with the click of a button at checkout.

This convenience has particularly attracted younger generations, who show lower adoption rates for traditional credit cards. The possibility of buying first and paying later has always existed, but turning this concept into a widely accessible digital tool was the sector’s great differentiator.

However, BNPL also presents challenges. The lack of rigorous credit checks, while facilitating adoption, may prevent consumers from building a solid financial history. Some companies have already started reporting data to credit agencies, and regulators in Europe and the US are assessing how requirements for this sector will evolve in the coming years.

Meanwhile, the model’s relevance has attracted major players like PayPal, Visa, and traditional banks. This creates even bigger challenges for fintechs in the sector, making the monetization model an even more strategic factor for their consolidation and permanence in the market.

To differentiate themselves, these companies will need to move beyond payments, providing data, strategic insights for merchants, and additional benefits for consumers. Klarna recognized this early and built an ecosystem that extends beyond payments, showing that, at the checkout of growth, creating an ecosystem that adds value for both retailers and customers can be a pathway to success.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://baymard.com/lists/cart-abandonment-rate

https://www.klarna.com/international/klarna-history/

https://sacra.com/c/klarna/

https://www.fool.com/investing/general/2013/04/03/the-slow-death-of-credit-cards.aspx

Excellent content, Walter, I really liked it, and will start reading your posts regularly. Greetings from Brazil! 🇧🇷