#3WiF: Payments are at the heart of the fintech industry, and Barte aims to be the artery that connects it all

W FINTECHS NEWSLETTER #120

👀 Portuguese Version 👉 here

What, When, Who in Fintech:

Today, I’m kicking off the 3W in Fintech series, where I’ll dive deep into fintechs that I believe are shaping the future of the industry, using three key criteria: strategies adopted, differentiation, and innovation. My goal is to provide clear and practical insights for investors and entrepreneurs, highlighting companies that stand out not just for their growth, but for their relevance and impact on the market.

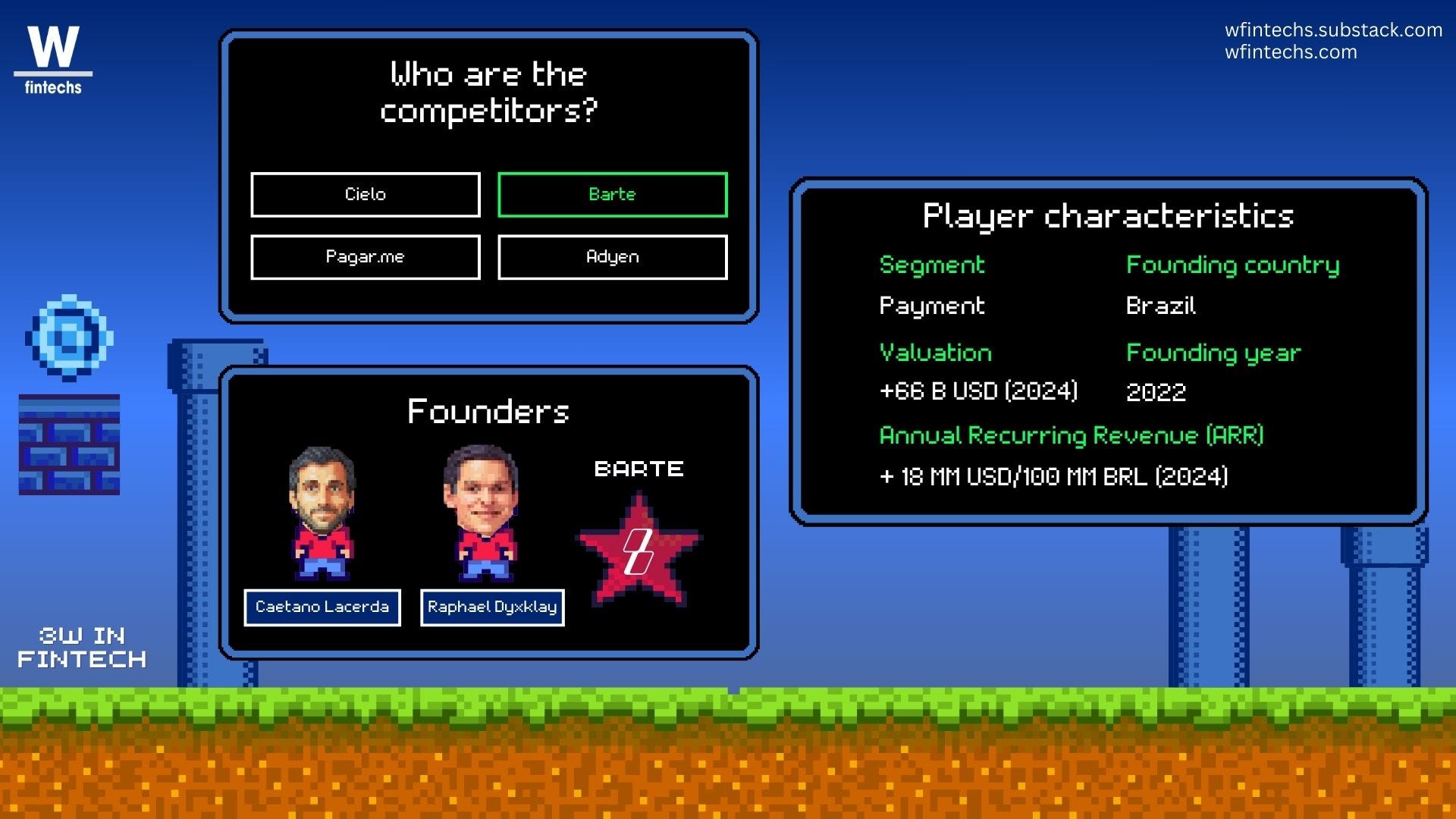

In this first edition of the series, I’ve chosen Barte, a Brazilian payment infrastructure fintech founded in 2022 and focused on medium and large businesses. The company grew from zero to BRL 100 million (approximately USD 20 million) in November 2024. Without chasing trends, Barte focused on getting the basics right. It has proven that to win in the market, you don’t need to create buzz — you just need to excel at what you do and deliver exactly what the customer truly needs.

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Payments are the heart of the fintech sector. Not only has it outperformed the S&P 500 and NASDAQ index in value growth over time, but it has also redefined global behaviors in ways few other segments have managed to achieve.

If we go back to 2010, payments were, without exaggeration, chaotic. Transferring money from New York to London was so slow that delivering it in person would have been faster. Paying for groceries often meant high transaction costs for merchants. Fast forward 14 years, and the landscape has completely transformed. We now have Pix, digital wallets, contactless payments, and payment initiation services. Today, money moves from point A to point B with a speed that has redefined expectations and an efficiency that would have seemed improbable in 2010.

The financial market tends to resist change, often due to strict regulations or complacency, prioritizing stability until external pressures force a shift. In Brazil, competition played that role. New players and technological demands pushed traditional institutions out of their comfort zones, accelerating the transformation that brought about innovation and the era of instant payments.

Despite recent regulatory changes, which I’ll briefly outline below, the market still holds significant opportunities and challenges that only it can address. Barte is actively working to fill these gaps in an already mature sector. This raises the question: Is there room for another player? Spoiler: The answer may lie in a combination of strategy, positioning, culture, and a lot of creativity — factors that help explain Barte’s impressive growth in just two years.

The before and after of the payments sector

Until 2010, Brazil's payments sector was dominated by two giants: VisaNet (now Cielo) and RedeCard (now Rede), which controlled 76% of all merchant establishments. These companies processed the majority of transactions from the 565 million cards in circulation in 20091. Meanwhile, card networks like Visa, Mastercard, and American Express controlled over 90% of credit and debit cards, creating a low-competition market.

Between 2003 and 2007, these acquirers saw their revenues grow by more than 300%, driven by the increasing use of cards and transactions. Discount rates were their primary source of revenue, while interchange fees represented their largest cost. The POS (card machine) rental model proved to be highly profitable, but its steep costs excluded small merchants from participating in the system2.

A study from 2006-2007 revealed that 73% of the variation in discount rates3 — the amount paid to process card payments — depended on the size of the business: large retailers were able to negotiate lower rates, while small businesses faced higher fees, creating an uneven market where smaller merchants were burdened by higher costs.

Each card was linked to a processing company controlled by the issuing banks. VisaNet, with Banco do Brasil, Bradesco, and Visa as shareholders, and RedeCard, connected to Unibanco, Itaú, and Citibank, processed 94% of transactions and 90% of the financial volume 4. Additionally, the lack of interoperability between card networks imposed restrictions: Visa cards only worked with VisaNet, and Mastercard cards only worked with RedeCard.

The only way out of this closed market, where a few controlled so much, was regulation. Since 2006, the Central Bank had been investigating the sector, in partnership with other agencies, to map out its flaws. The study, published in 2009, revealed the market concentration in VisaNet and RedeCard, the barriers to new players, and the lack of interoperability between card networks. The message was clear: urgent changes were needed to make room for competition.

The story after 2010

Competition arrived through reforms that reshaped the payments system, breaking the VisaNet and RedeCard duopoly and opening up space for new players. The Central Bank and competition defense agencies, such as CADE, began this process with an action from Abranet against RedeCard in 2014 for abusive practices that hindered access for digital facilitators like PayPal. CADE intervened, resulting in a BRL 7.45 million fine for RedeCard.

In 2015, the Central Bank took an important step with Circular No. 3,765, opening the payments market and allowing card networks like American Express to be accepted by acquirers such as GetNet, Rede, Cielo, and others. This broke the exclusivities, increased competition, and gave consumers more options. In 2017, an agreement between Itaú, Hipercard, and Rede, along with Cielo's involvement and the centralization of payments by CIP (Interbank Payments Chamber, responsible for coordinating transactions between banks), resulted in a more transparent and dynamic environment with more balanced conditions for all market participants.

These changes reduced the dominance of card networks like Visa and Mastercard, while new networks like Elo and acquirers like Stone and PagSeguro increased competition. After 10 years, the market share of the giants VisaNet (now Cielo) and RedeCard (now Rede) has melted away, dropping from 90% in 2013 to 45% in 2023.

The regulator's reform created the ideal environment for competition to thrive and, of course, for consumers to benefit. The initial strategy of some new players was clear: it was no longer possible to ignore small businesses. It was a perfect storm: merchants losing part of their profits to high fees and rented POS systems, technology rapidly evolving, and the regulator clearly stating that the old setup was no longer acceptable. That's when the new entrants saw the opportunity and began to capture the millions of underserved businesses.

New players

Among these new players, Stone and PagSeguro stood out. They understood that acquirers were focusing on large companies, offering complex solutions, while these fintechs turned their attention to small and medium-sized entrepreneurs. They didn’t just offer a payment option but a promise of simplification and accessibility — something the big players had failed to deliver until then. The market demanded practical, straightforward solutions for small and medium businesses, which represent nearly 30% of Brazil’s GDP and more than half of job generation in the country5.

Stone adopted an aggressive strategy and invested heavily, unafraid to challenge the industry. The acquisition of Elavon was one of these moves, driving customer base expansion and accelerating growth. The company quickly identified what was working and, more importantly, what others weren't doing: quality customer service and solutions tailored to the needs of small businesses. In addition, it built its own distribution network, which helped with expansion.

PagSeguro also found its niche by opting to sell POS terminals instead of renting them out, as the big players did. This was essential for microentrepreneurs, who, instead of paying high monthly fees, could purchase the equipment at a more affordable price. This eliminated recurring costs. UOL's support accelerated customer acquisition and solidified its position in the market.

The results of the reform, such as the interoperability between card networks and the centralization with CIP, allowing merchants to consolidate payments on a single machine, combined with the strategies adopted by the new entrants, led to the number of POS terminals growing from 5 million in 2012 to more than 20 million in 2022. Increased competition strengthened merchants' bargaining power, whether large or small. The result was a reduction in fees, including the Merchant Discount Rate (MDR) and the rental/purchase costs of POS terminals, as well as faster customer service and support.

Stock market performance

Despite the contributions both have made to Brazil’s payments market, the challenges faced by PagSeguro and Stone on the New York Stock Exchange clearly illustrate how macroeconomic factors and strategy execution can collide. Both are dealing with the pressure of high interest rates in Brazil, which directly affect their credit operations. Stone and PagSeguro have shown significant growth, but the cost of this success is becoming an increasingly difficult challenge. Stone, with a 664% increase in credit between 2022 and 2023 6, is grappling with the challenge of balancing accelerated growth and profitability. The increase in loans from BRL 113 million to BRL 864 million in one year is impressive, but the high interest rates have put pressure on their margins and increased the cost of capital.

PagSeguro has also been working with large retailers, especially those with monthly sales between BRL 1 million and BRL 30 million. In the third quarter of 2024, the total transaction value of this group was BRL 48 billion, a 62% increase compared to the previous year7.

Both companies are trying to build a bridge while crossing the river: necessary, but full of uncertainties. While they present strong results, they face the challenge of balancing rapid growth with rising capital costs and tighter margins.

Both Stone and PagSeguro have proven that innovation is not about creating something completely new, but about simplifying, customizing, and making what already exists more efficient. They challenged the industry giants and, of course, collected their own scars in the process.

If you're enjoying this edition, share it with a friend. This will help spread the message and allow me to keep offering quality content for free.

The arrival of Barte

It was against this backdrop and the new opportunities in the payments market that Barte reached a valuation of BRL 400 million in its latest funding round. A Portuguese and a Brazilian decided to take on both new and established industry giants, targeting medium and large businesses. Founded in 2022, the company chose the name inspired by the English concept of "barter," which means direct exchange, or "escambo" in Brazil. Since the term "escambo" is not common in Portugal, they opted for "Barte," keeping the same idea.

The company combines growth, a strong culture, and an offering that caters to a market increasingly hungry for flexible and personalized payment solutions. To understand what made Barte grow so quickly, it's essential to take a step back and understand the profile of its founders.

Founders

Caetano and Raphael didn't know each other, but they are the embodiment of what Steve Jobs stated in his famous Stanford speech: "You can’t connect the dots looking forward; you can only connect them looking backward." Raphael and Caetano connected through Marcela Giannella, a mutual friend who worked with Raphael and studied with Caetano. Caetano initiated the conversation via LinkedIn message, and soon both of them realized there was potential there.

In less than two weeks, they raised the pre-seed round for Barte. Without a fully formed thesis but with a strong team, they secured the investment, as early-stage funds tend to bet more on people than on fully developed ideas.

The story behind this deal is another example of how connecting the dots works. After leaving his last job, Caetano shared his interest in entrepreneurship with friends. At a party in Greece, a friend mentioned his idea to an investor present, leading to the first proposal for the round, from Venture Friends, which would become a major partner for Barte.

The founders' background is what made the fund believe in them. Raphael, who had already led teams in three Brazilian unicorns (Creditas, Loft, and Olist), and Caetano, with his experience at the British unicorn Tractable, gave the project the credibility it needed. Caetano once explained to Raphael why he was interested in Latin America: "It's incredible how much more friction my life has been since I moved to Latin America. Whether it's my banking app crashing, booking a flight with an international credit card, or even going through security to enter the office in the morning, the processes can be improved everywhere.8” This vision of the potential for disruption was one of the main reasons he chose Latin America, where the impact of entrepreneurship has a much greater transformative potential.

Their first physical meeting happened only after the investment round and Caetano's move from London to São Paulo. The connection that transformed the last three years of their careers was made virtually, without handshakes. In other words, sometimes it's only when looking back that we see how the dots connect.

In November 2021, Raphael sent me a message on LinkedIn. The message said:

"Hey bro, how’s everything going? I’ve started entrepreneuring again over here."

I met Raphael in 2019 through a colleague, and I was able to closely follow some of his moves and others as a spectator. What really stood out to me, and I believe is his biggest strength as an entrepreneur, are his adaptability and listening skills. In a world where everyone is more concerned with speaking well, Raphael stands out for “listening well.” He listens genuinely, absorbs, learns, and, if convinced, is willing to change his perspective. I believe his success comes from exactly that: his ability to absorb, learn, and, if necessary, relearn. Although he graduated in Literature, an area that may initially seem far from everything he has built, looking from the outside, I see that his frustration with the course and the intensity with which he sought to understand things deeply during his youth may have been fundamental. This relentless search to understand what lies beyond the surface shaped his active listening, a skill that has undoubtedly helped him get to where he is today.

I’ve interacted with Caetano only a few times over these 3 years at Barte, but it became clear that he shares with Raphael an analytical, observant, and practical profile. His experience in the European market brought a strategic vision that complements the company’s dynamic. Together, they were able to shape the culture of Barte, where the exchange of ideas without judgment is the core pillar. Creativity is undoubtedly one of the main rules of the game for Barte to navigate a market of giants. If the environment had been hostile or judgmental, the company probably wouldn’t have been as creative during several moments of its journey.

Culture

At the beginning of 2024, I was surprised by a LinkedIn post from Raphael. It was a post about the company’s culture, accompanied by a rich 40-page document. Barte, a relatively new company, was opening its “office” to the public. Undoubtedly, a great strategy to attract talent.

The document has four points that I believe are connected to the company’s growth:

Think of the company: “We don’t expect our members to work excessive hours or sacrifice their priorities outside of work. But we do expect them to wash the dishes thinking about how the company can be better.”

No politics: “The best talents can’t stand looking to the side and seeing people who generate less result being promoted due to affinities or knowing how to sell themselves better.”

Honest feedback: “We don’t want reality to be ‘filtered’ or ‘softened’ by leadership or anyone. From the director to the intern, we work only with adults and believe that everyone deserves transparency in both the good and bad news.”

Don’t try to create a Hollywood story, but solve problems: “A good team’s desire shouldn’t be for Hollywood-like events. On the contrary, a team needs to enjoy solving real problems in as boring a way as possible. Our scope is to generate value, not external impressions.”

In early-stage startups, it’s common to lack defined processes and communication failures, but Barte took a different approach. When I first read the document, it was clear that the effectiveness of a team, especially in the early stages of a business, is directly linked to the willingness of its members to get involved in different areas and learn by practice, solving problems.

Product strategy

Instead of inventing a new game, Barte has chosen to refine the rules, turning what seemed like a saturated field of established players into a space full of opportunities.

Caetano and Raphael understood early on that payments were more than just transactions, leading Barte to integrate payments and credit into a single ecosystem, expanding customers' purchasing power and eliminating bottlenecks like waiting for capital. While companies like Cielo, Rede, and Stone grew through acquisitions, facing integration difficulties and results below expectations, Barte opted to be omnichannel from the start, seamlessly integrating physical and digital experiences.

Looking at Barte's API documentation it’s clear that the focus is on the developer, with explanatory videos and dev-friendly language, which reminded me of Plaid's approach — I’ve commented on this strategy 👉 here. To further expand its solutions, Barte became a sub-accredited partner of Mastercard, allowing them to go beyond payment machines and Tap to Pay, with solutions like payment links and white-label options. In other words, they offer deep integration with customers' processes, turning payments into a strategic advantage for the business.

The contrast with companies like Stone and PagSeguro is clear. While these companies democratized access to payment machines for small businesses, struggling to scale solutions for medium and large businesses, Barte integrated different channels. While Stone and PagSeguro focused on mass retail, Barte positioned itself as the next chapter: a strategic infrastructure that turns payments into a competitive advantage for large businesses.

The company's business model is clear: it only earns when its clients win, charging a success fee per transaction. This creates an interesting dynamic, with rewards to encourage clients to reach their goals, similar to incentive programs for salespeople, but here, the "salespeople" are the clients themselves. The big difference is that, for Barte, the client is not someone to be served, but someone to be challenged. The vision goes beyond being a market leader; the goal is to explore the full potential of each client, ensuring that both grow together, as it is in this shared journey that both sides win.

In credit, Barte challenges itself through a partnership with Lend, a regulated company that handles all the bureaucracy related to accessing data from acquirers, registrars, and other factors in the credit process.

Barte then launched an option for clients to split their credit card purchases into up to 21 installments. The idea was to boost sales and help clients improve their cash flow, though the company was concerned that the cost of this service might not be worth it. However, surprisingly, nearly 30% of new clients chose Barte because of this installment option, and the company saw an increase in profit margins9.

The strategy worked well for many companies, with high credit approval rates and low price sensitivity among clients. However, it presented limitations. When installment payments on credit cards competed with options like loans, interest was lower. Additionally, for products under BRL 3,000, the cost of installments wasn’t justified. On the other hand, for customer segments like Housi, which sells property renovations between BRL 50,000 and BRL 150,000, installment payments proved to be an effective solution. The option to split payments into up to 21 installments increased the average number of installments from 1.4 to 7.3 in one year, showing great potential to drive sales and margins10.

Growth

Some of the numbers presented were extracted from the analysis by Rodrigo Fernandes, who also wrote about the company (link 👉 here).

This approach of challenging the customer, using payments as a pathway to something bigger, and aligning culture with creativity directly reflected in the company's growth.

Every well-managed startup knows that the priority of management should be to identify and understand the growth levers, directing energy to what truly matters. In other words, it is essential to understand where the business is heading and ensure that the assumptions are solid. Barte seems to have nailed these levers, although combining payments and credit is challenging. In credit, you have to build the bridge while crossing the river, meaning it’s an uncertain environment. Betting on medium and large companies, unlike some strategies of established players, seems to be a good alternative, as the margins are higher.

The company turned risk into a strategic advantage, which was directly reflected in its metrics. The LTV/CAC, which was 3 in August 2023 — meaning the profit generated per customer was three times the cost of acquisition — jumped to 17 in March 2024. Now, for every real spent on acquiring a customer, the company generates 17 reais in profit. They found a way to make operations more efficient and profitable: allowing customers to start with simple solutions, build trust, and as they grew, expand their options. This not only attracted new customers but also made the average revenue per customer grow 29 times since the first round of investments, leading the company to achieve BRL 60 million in annualized revenue. In November 2024, the company reached BRL 100 million in annual revenue, processing BRL 1.5 billion, and in three months, increased its customer base from 2,000 to 5,000.

Market positioning

What impresses me the most about Barte's story is its positioning. The sector, as I showed in the first part of this edition, is dominated by giants — whether through efficiency, capital, or political power. To compete, it’s not enough to just offer a better service. Creativity is key — and the company’s culture fosters this.

The company tested a Business Club to get closer to clients and prospects, creating a space to foster connections and business. However, this strategy involves some costs, such as the venue, food, and the time each member dedicates. It’s a common strategy among education players and fintechs, acting more as an engagement and visibility initiative than a direct conversion strategy. In other words, it strengthens the brand and cultivates relationships, but its immediate impact on sales results is limited.

Another strategy was on LinkedIn itself. Raphael realized that in a saturated market with ever-increasing positioning costs, the most efficient path would be to build a genuine community. That’s when he started producing more content on the platform, leveraging his presence to attract his own audience without depending on influencers.

The goal isn’t just to gain visibility, but to create a genuine connection. Each post aims to position Barte as the brand that customers want to see when paying for something, not out of obligation, but because they know the experience will be different. The strategy has been working, not only in generating leads but also in helping to unlock negotiations and increase the chances of closing big deals, turning LinkedIn into a key channel in the company’s sales funnel.

The campaign at Congonhas Airport, during the pre-holiday period of October 12, 2024, is an example of how branding works at the top of the funnel. At this stage, the focus isn’t on selling immediately, but on generating recognition and interest. The idea is to reach a broader audience and make them identify with the brand’s proposal, without rushing to close deals. That’s how they launched the “#ChamaABarte” campaign. Instead of focusing on quick conversions, the company chose to make an appearance to the public.

Adopting the "build in public" strategy, sharing both challenges and achievements, allows Barte to go beyond just a sales pitch. It is, in fact, cultivating trust and loyalty within its audience, creating a genuine connection. At this point in the branding journey, I see that the strategy is consolidating and becoming an important lever for differentiation in the sector, something that could be a significant edge in such a competitive market.

A artery that connects everything?

Barte believes it’s playing a generational game — it’s part of one of the payment generations. It makes sense. The first generation was dominated by incumbents, a duopoly that, as I showed, was only undone with regulatory intervention. In the second generation, the focus shifted to small and medium-sized businesses, where the gaps were clear, and the opportunities easier to identify and scale. PagSeguro and Stone carved out their space, but not without collecting scars in the stock market.

Now, in the third generation, the scenario has changed. I believe the focus will be on filling the gaps left by the companies from the two previous generations of payments, incorporating variables that emerged over time thanks to technology — something that the previous companies still struggle to address with agility.

Barte is betting on medium and large businesses, which were once the favorites of incumbents but are now leaving money on the table and demanding faster and smarter solutions. While incumbents have tried to adapt, companies that emerge without the baggage of an established culture tend to be more agile. The third generation is very much involved in what I mentioned in edition #114: payments are the primary channel that feeds data generation for personalization. So, the key is how to use technology and data to solve problems efficiently. And Barte has been doing this very well, tracking the flow of money and offering credit.

As I was thinking about the title I’d give to this edition, it soon came to mind that if payments are the heart of the fintech sector, veins and arteries are the channels through which blood circulates. The difference between them lies in direction: the vein brings the blood back to the heart, while the artery distributes it to the body. And this is where Barte comes in: with a strategy aimed at being a flexible payment infrastructure, it was born in this segment but is evolving into something much larger. If the need is credit, Barte answers; if the demand is for personalized solutions for the customer, Barte will be ready. In the end, Barte could be the artery that connects everything.

💡Bring your company to the W Fintechs Newsletter

Reach a niche audience of founders, investors, and regulators who read an in-depth analysis of the financial innovation market every Monday. Click 👉here

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://www.bcb.gov.br/pom/spb/seminarios/2010_seminterncartoespagamento/arquivos/cndl.pdf

https://www.bcb.gov.br/content/estabilidadefinanceira/Publicacoes_SPB/Relatorio_Cartoes.pdf

https://www.bcb.gov.br/content/estabilidadefinanceira/Publicacoes_SPB/Relatorio_Cartoes.pdf

https://www.bcb.gov.br/content/estabilidadefinanceira/Publicacoes_SPB/Relatorio_Cartoes.pdf

https://exame.com/pme/as-pmes-representam-27-do-pib-confira-dicas-para-ter-sucesso-na-sua_red-01/

https://api.mziq.com/mzfilemanager/v2/d/46ed7b29-1318-408a-a036-ba544e2ecccb/ae409361-5429-9c8f-b29a-932052fcbdac?origin=1

https://api.mziq.com/mzfilemanager/v2/d/d1c190f7-52c1-4663-aa9f-0e0141aa5e3c/e2d52b19-c4b1-1b45-5c07-953f630cdfa8?origin=1

https://www.linkedin.com/pulse/product-market-fit-latin-america-raphael-dyxklay/

https://www.linkedin.com/posts/rapha-dyxklay_n%C3%BAmeros-de-bastidores-menos-de-10-das-activity-7221483808842272768-0bM0?utm_source=share&utm_medium=member_desktop

https://www.rodrigofernandes.io/barte-pagamentos-midmarket