#FintechFrames: Wise turned the distance between two points into a cross-border payments infrastructure

W FINTECHS NEWSLETTER #138

👀 Portuguese Version 👉 here

Fintech Frames — Edition #02

Fintech Frames is a series by the W Fintechs Newsletter highlighting the journeys and strategies of fintech companies that have established themselves in the market — whether through an IPO, acquisition, or a valuation exceeding $10 billion.

Other editions Fintech Frames

For those looking for stories of founders still in the early stages, 3W in Fintechs dives into the beginnings of many ventures. Click 👉 here to explore all editions.

👉 W Fintechs is a newsletter focused on financial innovation. Every Monday, at 8:21 a.m. (Brasília time), you will receive an in-depth analysis in your email.

Over two thousand years ago, Euclid laid the foundations of geometry by stating that between two points, it is always possible to draw a straight line — the shortest distance between them. Today, we could say that Euclidean fintechs have emerged: companies that shorten the time between economies, not through straight lines, but through technology.

The evolution of cross-border payments has turned an ancient mathematical truth into a new logic for global exchange. It's no longer about the shortest distance, but about the shortest time. Two points on the globe — São Paulo and London, for instance — are still separated by kilometers, currencies, time zones, and banking systems. But now they connect in milliseconds. Technology hasn’t shrunk the planet, but it has drastically reduced the time needed to move across it — something journalist Thomas Friedman foresaw back in 2005 in his book The World Is Flat.

Over the past two weeks, I’ve been analyzing several cross-border players. The most interesting infrastructure thesis I found was Wise’s. The company managed to build something with significant impact — not only for customers but for itself as well. The numbers speak for themselves: in 2024, Wise had 12.8 million active B2C customers and 625,000 B2B customers, with revenue surpassing £1 billion.

Unlike many players in this space, Wise’s strategy combines local banking licenses, its own accounts in dozens of countries, and a parallel infrastructure that lowers costs and speeds up settlement. Instead of relying on the traditional global network, Wise created its own web of interconnected domestic transfers — and turned that into its biggest asset.

This approach not only delivered faster and more transparent experiences to users, but also allowed Wise to operate profitably, even while offering fees well below market rates. The key lies in how the company reimagined the logic of payments: not as a bridge between banks, but as a continuous flow of synchronized local settlements.

In the first edition of Fintech Frames, I explored Klarna’s model and how it redefined credit. By building bridges between B2C and B2B, Klarna developed an integrated ecosystem of data, credit, and services.

In this edition, readers will quickly notice how Wise has redefined the logic of cross-border payments by prioritizing transparency for both B2B and B2C customers. Still, there’s a vast field of opportunity yet to be explored — especially when it comes to the use of stablecoins, which could make the system even faster, cheaper, and more efficient, as some players in the market are already demonstrating.

From TransferWise to Wise

In ancient trade, thousands of years ago, wisdom was about reducing the friction involved in a transaction. From salt to paper money, our ancestors were wise in finding ways to make exchanges smoother. In many ways, the story of Wise carries that same principle forward.

When Taavet Hinrikus and Kristo Käärmann founded TransferWise in 2011, their motivation was simple: to make international money transfers fairer and more transparent. They were both personally affected by the hidden costs and delays of traditional banking systems. As expats living and working in different countries, they constantly needed to send money back home.

Taavet, the first employee at Skype, was living in London but being paid in euros from Estonia. Kristo, on the other hand, worked in London but needed to pay his mortgage in Estonia1. Every time they made international transfers, they noticed that banks would advertise “zero fees” or “official exchange rates,” but would sneak in hidden markups and take days to complete the process.

That monthly frustration led them to create a faster, fairer, and more transparent solution.

The traditional path of money transfers

Wise entered a deeply complex market. Sending money across borders is still — in most cases — slow, expensive, and lacks transparency. The dominant infrastructure relies on the correspondent banking model, coordinated by a network called SWIFT (Society for Worldwide Interbank Financial Telecommunication), founded in Belgium in 1973.

Despite its reliability and scale — today connecting over 11,000 institutions across 200 countries and handling around 50 million messages daily2 — SWIFT doesn’t actually move money. In practice, it acts as a messaging system: one bank notifies another that a specific amount should be sent to a particular account in a different country. For the funds to actually move, banks must maintain correspondent relationships — that is, accounts with one another or with intermediaries.

This setup requires each bank to establish bilateral relationships with institutions in many countries. Since few banks have a truly global footprint, a single transfer often involves three to five intermediaries — the sending bank, one or more correspondent banks, and the receiving bank. Each intermediary charges a fee and adds time to the process.

This is where hidden fees and exchange rate spreads come into play, making it hard for the average user to understand the true cost of a transfer. Many banks advertised “zero fees” or “official exchange rates,” but would hide a markup in the exchange rate — often ranging from 3% to 6%, depending on the currency and destination.

This structural misalignment opened the door for a new generation of faster, more transparent, and more accessible solutions. In recent years, even SWIFT has tried to modernize with initiatives like SWIFT gpi (Global Payments Innovation), which improve traceability and speed for certain transactions. Still, the rise of new infrastructures — like local instant payment systems (Pix (Brazil), UPI (India), Faster Payments (UK)) and more recently, blockchains and stablecoins — has brought faster and cheaper alternatives to the table.

Transfer = Wise

By building its own network of local accounts and applying the real exchange rate with clearly stated fees, Wise was able to cut out intermediaries — reducing costs and bringing more predictability to the user experience.

In 2021, the company dropped “Transfer” from its name and became simply Wise, marking a strategic shift. It was no longer just a transfer alternative — it was positioning itself as a global platform for moving and managing money across multiple currencies. Wise began offering international IBAN accounts, debit cards, interest on balances, and an open infrastructure for banks and fintechs to integrate with — reinforcing its vision of building the “ultimate network for the world’s money.”

If you're enjoying this edition, share it with a friend. This will help spread the message and allow me to keep offering quality content for free.

The Infrastructure Strategy

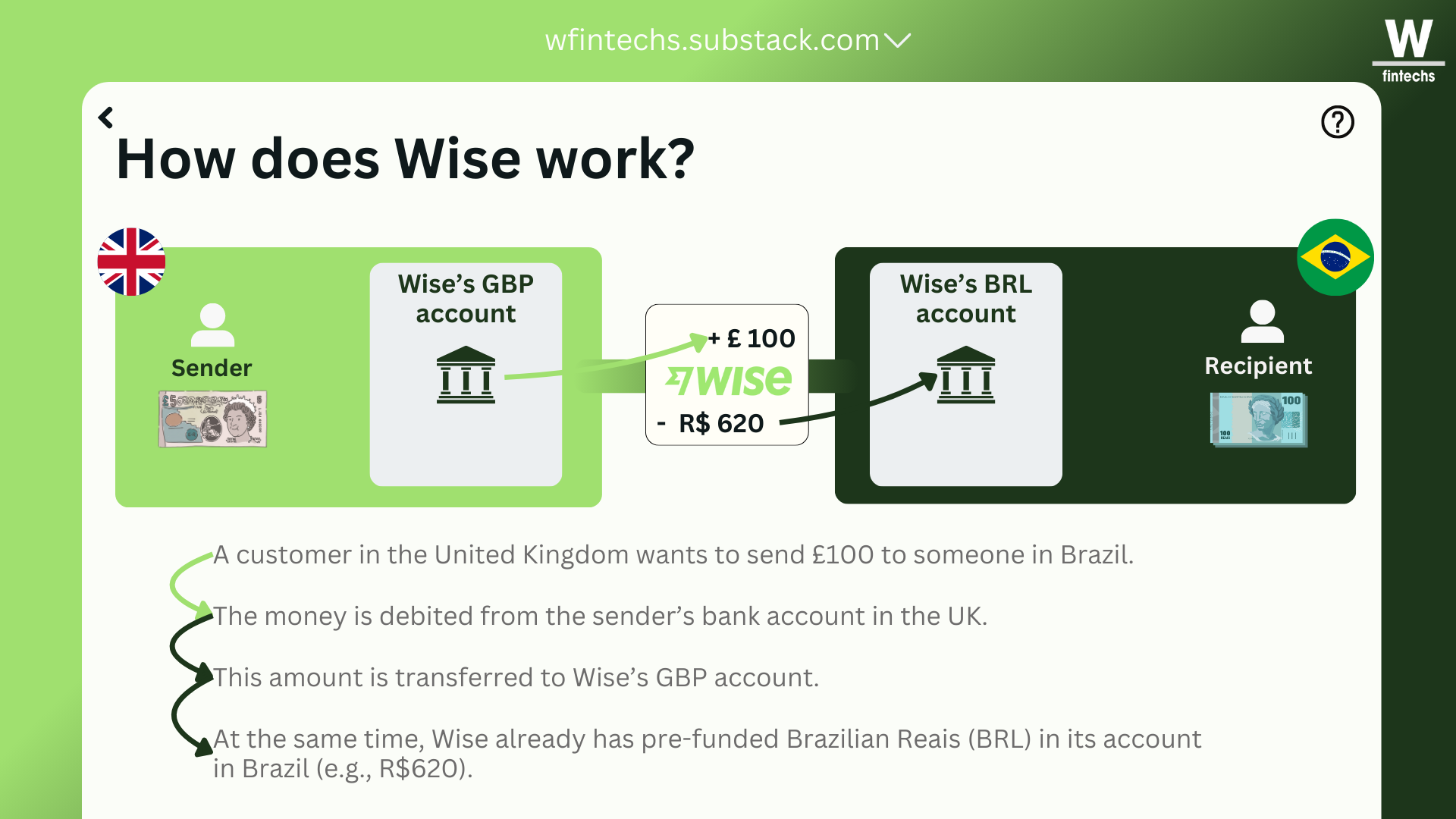

Wise’s vision of building the “ultimate network for the world’s money” has allowed it to innovate at speed. Rather than physically moving money across borders for each transfer, Wise holds pre-funded liquidity in local bank accounts across more than 40 currencies.

When a customer sends money, the funds are effectively “moved” within the same country — for example, a payment in pounds is received in the UK and immediately offset by a payment in Brazilian reais from Wise’s local account in Brazil. In other words, money doesn’t actually cross borders — it’s settled locally using funds Wise already holds in each country. This dramatically reduces cost, time, and complexity.

To make this operation viable at scale, Wise has been securing regulatory licenses in multiple countries. At first glance, its public reports don’t fully reveal the company’s expansion strategy — but a closer look at its activities in Brazil, Japan, and the U.S. shows a clear pattern.

Today, Wise holds more than 65 licenses across 45 countries. In the U.S. alone, it operates under authorizations in 49 states and has three dedicated subsidiaries to manage assets and integrate infrastructure (Wise Platform). The principle guiding this approach is clearly stated in some of its annual reports:

“As we build our presence, we deepen our connection by obtaining our own regulatory licences.” 3

In short, wherever it makes sense to operate, Wise secures a license and builds the operation from the ground up.

In Japan, for example, Wise obtained one of the country’s most difficult licenses in 2024 — the Type 1 Funds Transfer Service Provider license. In Australia, it operates under a local license with direct access to the NPP system. In countries like India, Indonesia, Mexico, the Philippines, and South Africa, it established its own subsidiaries to gain greater freedom to operate. In Brazil, it started with multi-currency accounts and money transfers and is now moving toward full integration with Pix.

The markets where Wise operates are highly relevant — a key factor behind its expansion thesis. In Brazil, around USD 2.83 billion in international remittances were processed in 2024 across the market. Mexico exceeded USD 64 billion in the same year. With volumes like these, it makes perfect sense to offer personal accounts, business products (Wise Business), and even enable other platforms to plug into its network via Wise Platform.

Since Wise operates under a pre-funded liquidity model, it needs to position money in advance across multiple currencies and local accounts to guarantee liquidity and speed. This only works in markets where transaction volumes justify the investment. In smaller markets, Wise either partners with local banks or relies on offshore currency exchange, which involves slightly higher spreads.

This infrastructure allows each direct connection to cut out intermediaries — reducing costs and enabling near-instant transfers: 62% of transactions are completed in under 20 seconds, 83% in under an hour, and 95% within 24 hours.

What’s most interesting about Wise’s philosophy is that the company has managed to share its infrastructure with third parties — a concept embodied in what it calls the Wise Network. This has clearly become its most strategic and valuable asset, as it combines: (i) local connections to financial systems; (ii) proprietary regulatory infrastructure; (iii) in-house technology; and (iv) a globally consistent user experience. This is the foundation for Wise Platform, which allows banks and fintechs to integrate Wise’s infrastructure into their own services — a model similar to Banking-as-a-Service, but focused specifically on global transfers.

The numbers and culture behind the thesis

The business model Wise chose requires patience and capital — but the results are already clear. The company has shown steady growth in its customer base (up 29% in 2024), while transfer volumes increased by 13% compared to 2023, moving approximately £118.5 billion in international transactions. All of this was achieved with a lean marketing budget, as two-thirds of new customers come through referrals.

Wise now serves 12.8 million active customers, including 625,000 businesses. More than half of them use the Wise Account, which allows users to hold and move money in multiple currencies while earning interest on their balances. The growth in the B2B segment is particularly notable: business transfers now account for nearly half of total volume, with the average B2B customer transacting seven times more than a typical B2C user.

Wise’s obsession with user experience is so strong that in several investor presentations, company executives emphasize that their biggest competitive advantage isn’t just lower pricing — it’s the fact that users know exactly what they’re paying for.

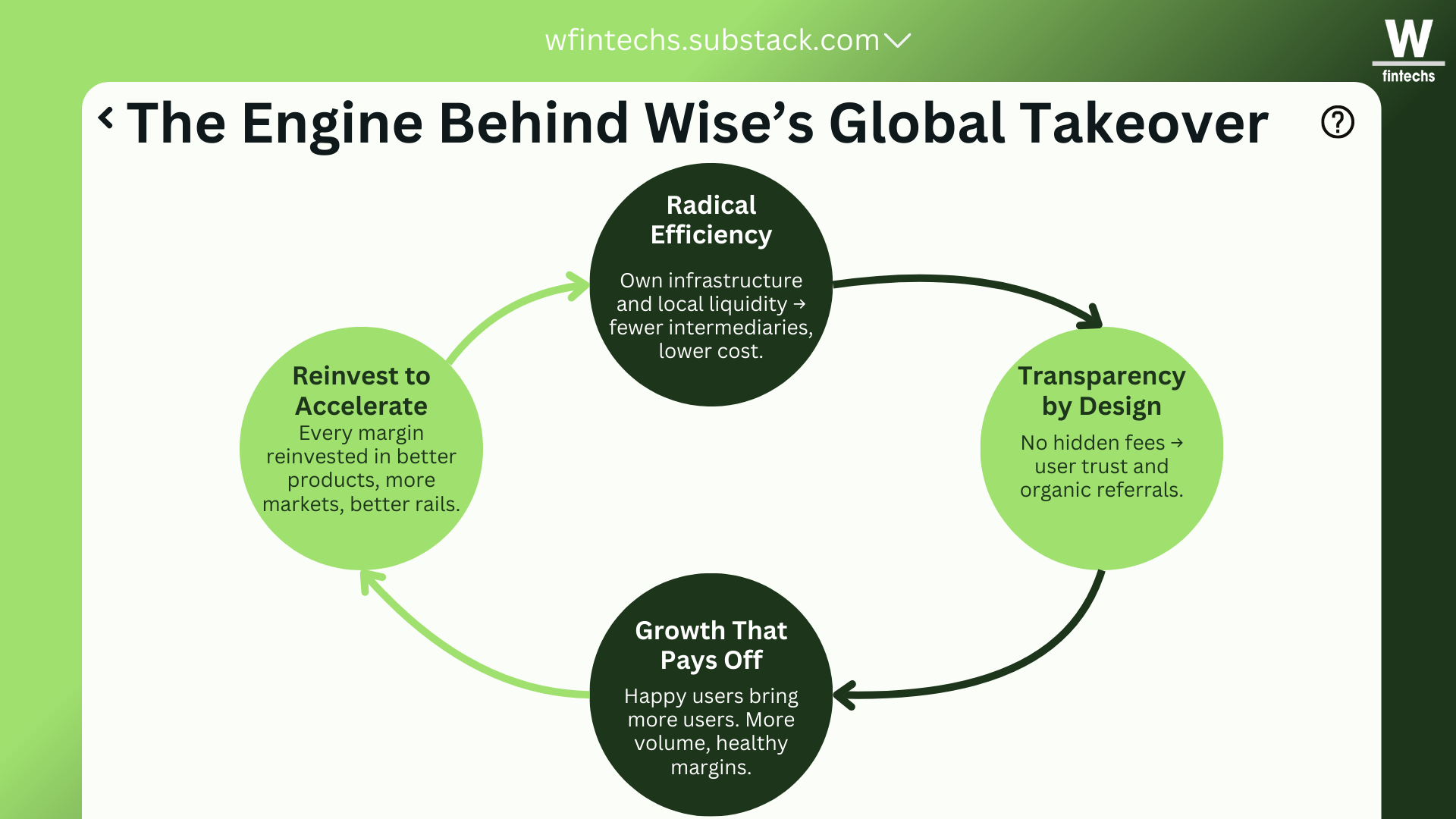

This efficiency isn’t just about profitability — though the company reported £481.4 million in profits in 2024. It also fuels a virtuous cycle: stronger margins allow Wise to reinvest in new markets, lower prices, and improve its products, which in turn attracts more customers and drives greater scale.

👉 Subscribe to W Fintechs and receive an analysis like this in your inbox every Monday.

Is the next era of cross-border will be Wise?

True wisdom has always walked hand in hand with transparency. Socrates, in his dialogues, was so transparent in his way of thinking that Plato immortalized them. Jobs’ wisdom lay in anticipating desires — and his version of transparency was turning vision into something clear and shareable, inspiring those around him to make it real. Wise’s wisdom lies precisely here: not just in making international payments instant, but in being transparent in a market where complexity has long served as a veil for hidden fees and high spreads.

Wise belongs to a generation of companies that chose to move away from the traditional model of international transfers and instead build their own global payment networks. This shift enabled lower costs, faster transfers, and a far more transparent user experience.

But it’s not alone. The rise of stablecoins like BRLA, USDC, and USDT points to a similar path: instant settlement, borderless, and without intermediaries. Models like stablecoin-based settlement are already being tested by players such as Visa, Stripe, and several banks — bridging the fiat world with on-chain systems through smart contracts.

For a company like Wise, which already operates with pre-funded liquidity and a relentless focus on transparency, adopting stablecoins seems like a natural evolution of its business model. Adding stablecoins as another settlement rail would allow Wise to maintain end-to-end control of the user experience — but with even more speed, flexibility, and global reach. Especially in markets where local infrastructure is still limited, this opens up new possibilities for Wise Platform and the B2B segment.

Wise shortened the distance between two points — not with a straight line, as Euclid once defined, but through a transparent cross-border payments infrastructure.

If you know anyone who would like to receive this e-mail or who is fascinated by the possibilities of financial innovation, I’d really appreciate you forwarding this email their way!

Until the next!

Walter Pereira

Disclaimer: The opinions expressed here are solely the responsibility of the author, Walter Pereira, and do not necessarily reflect the views of the sponsors, partners, or clients of W Fintechs.

https://www.bbc.com/news/business-46985443

https://stripe.com/br/resources/more/international-payments-101-what-they-are-and-how-they-work

https://wise.com/imaginary-v2/images/5321e97865fc73e1f23350600a70525b-WIS004_23ARA_BOOK.pdf