#31: What's the impact of fintechs in Brazil?

W FINTECHS NEWSLETTER #31: 06/12-12/12

Hi everyone 👋,

In this edition of W Fintechs I’ll talk about:

Settings of our market

Some metrics of our fintech market

👉W Fintechs is a newsletter about fintechs, every Monday at 8:21 a.m. you’ll receive an email about insights and happenings in the universe of fintechs — I usually write in Portuguese.

Commonly, people say that the impact of a particular industry can be measured by the size of the market, the investments, and what that industry does to people's lives.

For the fintechs industry, these metrics work really well too. When we realize the maturity of this sector, we see a full impact on people's lives.

Through API Economy, fintechs were able to go faster and create customer-centric solutions. Here in Brazil, we could see a big disruptive movement in financial services with fintechs as leaders. Until 2015, for example, Brazil's leading private bank Itaú had a good part non-tech approach 1 — although this company has led the digital movement in the past, fintechs excelled in speed over traditional banks.

Today, traditional banks and fintechs are changing our banking experience — we have more options to choose from. It's competition at its best. The Brazilian financial market has large movements, both in investments and in M&As.

A little bit about settings of our market

A few editions ago, I discussed how our insurance market works [available in English here]. At a certain point in our financial history, the government and banks believed that it would be better to have some big companies in the financial sector — in short, they believed that if we had big banks, through Mergers and Acquisitions, it would result in a stronger financial sector.

However, in recent decades, the basic configurations of this market have not worked very well. David Vélez said in an interview that when he arrived in Brazil he tried to open a bank account and came across a terrible experience — queues, a lot of demand for documents, etc. When he compared this experience with the high profitability of the sector and low financial inclusion, he saw that there was a great opportunity to build a business initiative.

Since then, companies such as Nubank, Next, Inter, C6 Bank, Neon, Mercado Pago and small and medium fintechs are building a new phase in our financial history.

Some metrics about our fintech market

Market Size

As the first fintechs emerged in Brazil, we could see a relevant emergence of new players in this market. According to Distrito, a good part of Brazilian fintechs started from 2016. However, it was in 2017 that the Central Bank of Brazil started direct talks with the sector (with segment leaders, specifically) to create a more favorable regulation.

Data from Fincatch, TripAdvisor for fintechs, show that in Brazil we have more than 1,400 fintechs and they are distributed among: Business Management (19.85%); Payments (13.98%); Credit (13.23%); Digital Accounts (6.48%).

The trend is that with the strengthening of investments and increasingly favorable regulation (Open Finance, for example), more fintechs will appear over the next few years.

Impact on people’s lives = Adoption

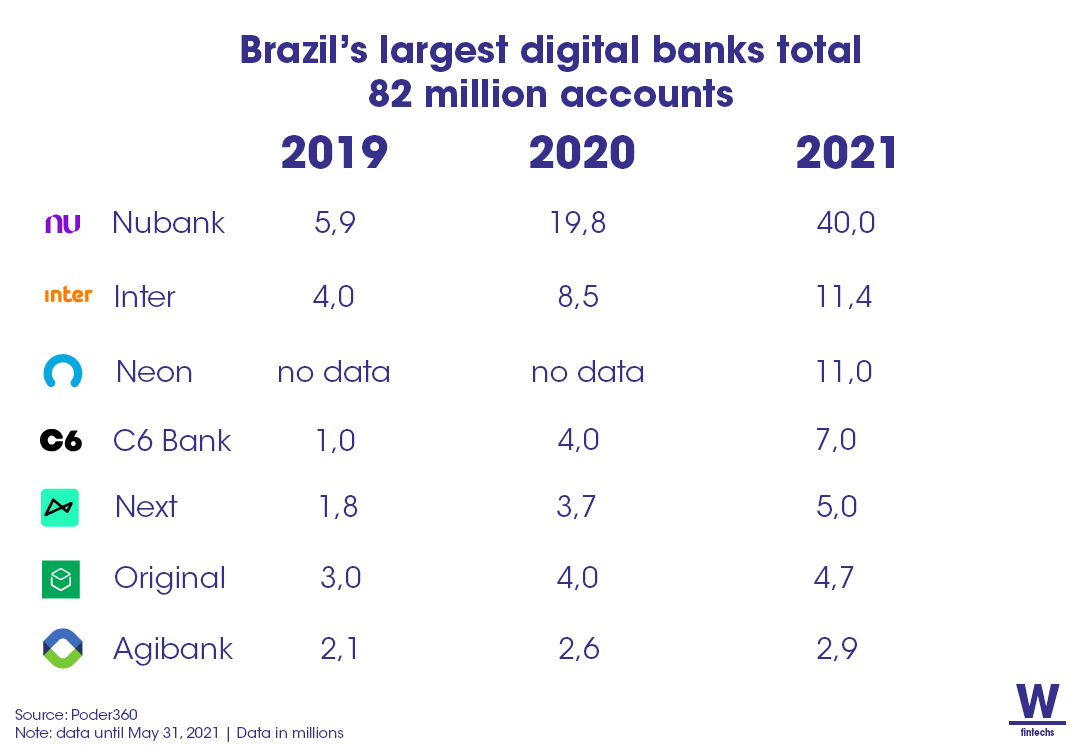

According to a survey carried out by the news portal Poder360, the largest digital banks total 82 million accounts.

Considering the 6 fintechs that released data from past years, there were 14.8 million accounts in 2019. The number is up 299% so far. Only Banco Original and Agibank did not double in size. Even so, they increased by 56.7% and 38.10% in the period, respectively.

In a report published by Nubank in August this year, the data show that there was a direct positive impact on customers, with improved financial inclusion and financial well-being, in addition to a macroeconomic impact that, according to the report, can be attributed to the benefits brought by Nubank.

According to the report, around 3.8 million Brazilians were included in the financial system for the first time through Nubank's services. 67% of customers who participated in the survey say they have achieved more financial independence through Nubank; 77% say Nubank has positively impacted their financial lives; and 87% indicate that, in the last 12 months, they managed to keep their finances under control and without large debts.

Investments

Our innovation ecosystem is getting more and more remarkable. In the first three months of 2021, Venture Capital investments already surpassed Private Equity investments.

So far, USD 11 Billion has been invested in the Brazilian startup ecosystem. Fintech leads the ranking. In November alone, more than USD 311 mi were invested in Brazilian fintechs.

As we have more fintechs standing out globally, like C6 Bank and Nubank, investors are attracted to our market.

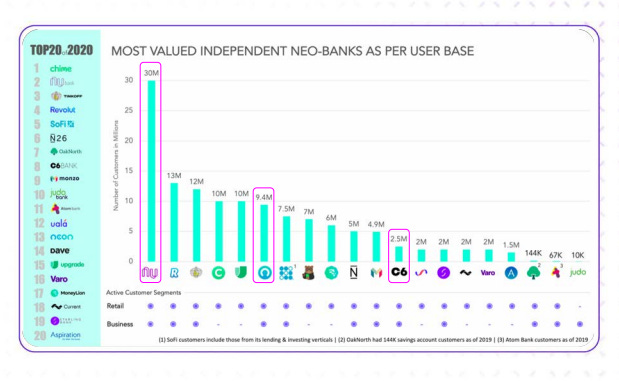

A study by WhiteSight found that among global fintechs Nubank is the largest neobank in terms of base size. C6 Bank also stood out for being the second digital bank to achieve unicorn status faster (2 years and 10 months).

Another movement in our market is M&As. In Brazil, financial and non-financial companies are incorporating some fintechs into their business strategies. Recently, software company Omie acquired the digital bank focused on SMEs, Linker, in a product expansion strategy.

Magalu, one of the largest ecommerce companies in Brazil, acquired Hub Fintech, a BaaS company, to expand its financial products. Cashback company Méliuz also acquired two fintechs, Alter (Cryptocurrency bank) and Acesso Bank (digital account), in a strategy to expand its financial line.

Moreover, with the astronomical growth of digital banks, the Brazilian financial market is faced with companies from other segments offering their own technologies to their customers. Such as iFood (with Movile Pay), Peixe Urbano (with Peixe Pay), GPA (with banQI).

Conclusion

The impact of the Latin American innovation ecosystem is catching the world's attention. I like the remark made by Mariano Gomide de Faria, co-founder of the Brazilian e-commerce company VTEX, where he says that "from a commodities exporter, we are becoming technology exporters".

Financial innovation in Brazil has impacted and will impact even more lives. As more players become unicorns, greater are the chances of these companies’ impacts on Brazilian society. Nubank is a good example of impact — by including 3.8 million people in the financial system. Niche fintechs segment such as CondoConta (digital bank for condominiums), ElasBank (digital bank for women), NG.Cash (digital bank for young people) and Conta Black (digital bank for black people) are also doing an excellent job of impacting positively a specific audience.

A new financial phase is being written — by the entrepreneurs and with the support of the regulators. The future will certainly be prosperous.

Until the next!

Walter Pereira

Thank you for reading to the end! If you liked it, I invite you to share🚀

https://a16z.com/2021/04/13/latin-america-fintech/